I. Introduction

Throughout the fiscal year, estimates of key budgetary measures such as revenue receipts, expenditures, deficits, and capital transactions fluctuate, impacting the implementation of vital schemes by both central and state governments in India. Achieving accurate estimates poses a significant challenge. In budget formulation and discussions on public economics, Budget Estimates (BE) and Revised Estimates (RE) are pivotal, awaiting the arrival of actual figures for macro-fiscal indicators. Traditionally, Indian states unveil their annual budgets and BE around the Union Budget presentation day (1st February), with RE becoming available towards the fiscal year’s end. Actual figures typically emerge approximately a year after RE, while they are accessible about two years after BE. The BE offers a projection at the fiscal year’s onset, setting the trajectory for subsequent financial planning.

This paper investigates potential biases inherent in BE and RE compared to actual figures within the above context. This analysis aims to assist policymakers in selecting between these two measures for further examination until actual data becomes available. Specifically, the study focuses on the Gross Fiscal Deficit (GFD), a crucial macro-fiscal indicator, using state-wise Indian data from 2006 to 2020. It identifies a systematic bias in RE compared to BE, prompting a recommendation for policymakers and researchers to rely on BE as an interim measure for macro-fiscal analysis across Indian states when actual GFD figures are unavailable. This preference for BE stems from its superior ability to approximate the actual GFD.

This paper builds on the two notes published by the Reserve Bank of India (RBI) in its 2020-21 and 2022-23 reports of “State Finances: A Study of Budgets”. There is a bias in the RE compared to BE and Provisional Accounts (PA) of GFD. Therefore, BE and PA can be used for policy analysis instead of RE (Reserve Bank of India, 2020). Using statistics, such as Mean Error, Mean Absolute Error, Root Mean Square Error, and Theil’s U statistics, a recent study finds that errors are higher in RE than in BE (Reserve Bank of India, 2022). Barring the two studies of RBI, the literature addressing the controversy about RE and BE is limited in India.

The RBI (2020) is a panel study of 24 Indian states for 2014-2019, and the RBI (2022) study estimates the bias considering 2017-2020. These studies need an extended time frame to draw any concrete conclusions regarding the bias in the RE and BE of GFD. Furthermore, these studies need more clarity on the selection of 24 states. However, we examine the nature of bias in RE and BE in two different panels of states, 17 non-special and 11 special states, for a longer timeframe, 2006-2020. The extended timeframe enables us to assess biases effectively compared to the two RBI studies. Therefore, our study can potentially fill the gap in the empirical literature that assesses the bias in the RE and BE of GFD in India. For ease of temporal comparison and consistency, we start our analysis from 2006-07, the post-period of the Fiscal Responsibility and Budget Management (FRBM) Act in India. The FRBM was effective from July 5, 2004. We believe the period after FRBM will likely differ from the pre-FRBM period in terms of the government’s taxation and spending behaviour.[1]

The rest of the paper proceeds as follows. Section II briefly discusses the political economy of fiscal deficit. Section III demonstrates the data and method used in the paper. Section IV discusses the empirical results. Section V concludes the paper with some policy implications.

II. Political Economy of Fiscal Deficit in India

Fiscal deficit measures the government’s borrowing needs for a budget year to finance expenditures, including interest payments. Standard economics claims that fiscal deficits are a consequence of consumption smoothing efforts by the government (Barro, 1979). However, deficits are inevitable in economic contractions owing to reduced tax collection when the government maintains a steady flow of expenditure and tax rates to facilitate smooth consumption. In many instances, governments amass debt beyond levels that could be explained by consumption smoothing theories (Alesina & Perotti, 1995). Here, possible new explanations of fiscal deficits, such as political factors, are warranted. The political economy of fiscal deficit gives a perspective on the bias inherent in BE and RE of the deficit. In the interest of brevity, the influence of political considerations on fiscal policymaking can be summarized as follows.

First, political economy posits that conflicts of interest affect deficits. This strand of literature is based on the principle that voters make consistent mistakes where fiscal illusion plays a central role. The three fundamental elements of fiscal deficits are the outcome of opportunistic politicians as follows. Opportunistic policymakers target votes for themselves or their parties and are prone to tilt economic policy to realize that goal. In many instances, voters value public expenditure for the direct impact of government programmes or the expansionary outcomes of expenditure hikes. In this approach, voters are assumed to fall into the trap of ‘fiscal illusion’; that is, they consistently underestimate the future costs of current spending programs (Buchanan & Wagner, 1977). Nordhaus (1975) also supports the framework of opportunistic politicians generating deficits to win elections at the cost of the general welfare.

Second, policymakers have diverse partisan preferences. The incumbents choose to run deficits because of divided interest among politicians’ partisan preferences. The fiscal deficit arises if politicians have diverse fiscal preferences. The argument that incumbent officials prefer deficits to limit their successor’s financial management freedom is plausible. This argument rests on the hypothesis that current budget deficits impose costs in terms of reduced future public spending or increased future tax collections (Alesina & Tabellini, 1990). Later, Alt & Lassen (2006) popularised models of strategic deficits based on politicians’ heterogeneous preferences about the structure of public expenditure.

Third, disagreements of interest between social groups or regions produce tensions in distributing government resources, resulting in overspending. Studies show deficits owing to the conflict between groups with diverse expenditure preferences over the allocation of government revenues. Theoretical inputs within this branch of the literature link fiscal outcomes to the nature of the electoral system, democracy types, and the degree of cohesion or fragmentation within the government.

Given this snapshot understanding of possible causes of fiscal deficit, this paper does not claim to explore any reasons for the deficit, albeit the paper restricts its purview only to the empirical assessment of the two measures of GFD: RE and BE.[2]

III. Data and Methodology

A. Data

We use the GFD, calculated as a percentage of Gross State Domestic Product (GSDP), data from 2006-07 to 2020-21, provided by the Budget Documents of various state governments and the Comptroller and Auditor General (CAG), Government of India. We focus on the 17 non-special category states, which are considered to be the major Indian states in terms of the size of the economy. However, the 11 special category states are also considered to buttress our main finding.[3] Telangana is excluded from our analysis since our period starts from 2006-07, and this state came into existence in 2015-16. GFD is the aggregate expenditure (aggregate disbursement net of debt repayments) minus revenue and non-debt capital receipts. We calculate two gaps, Gap1 and Gap2 of GFD as follows:

Gap1=Actual Estimate−BE

Gap2=Actual Estimate−RE

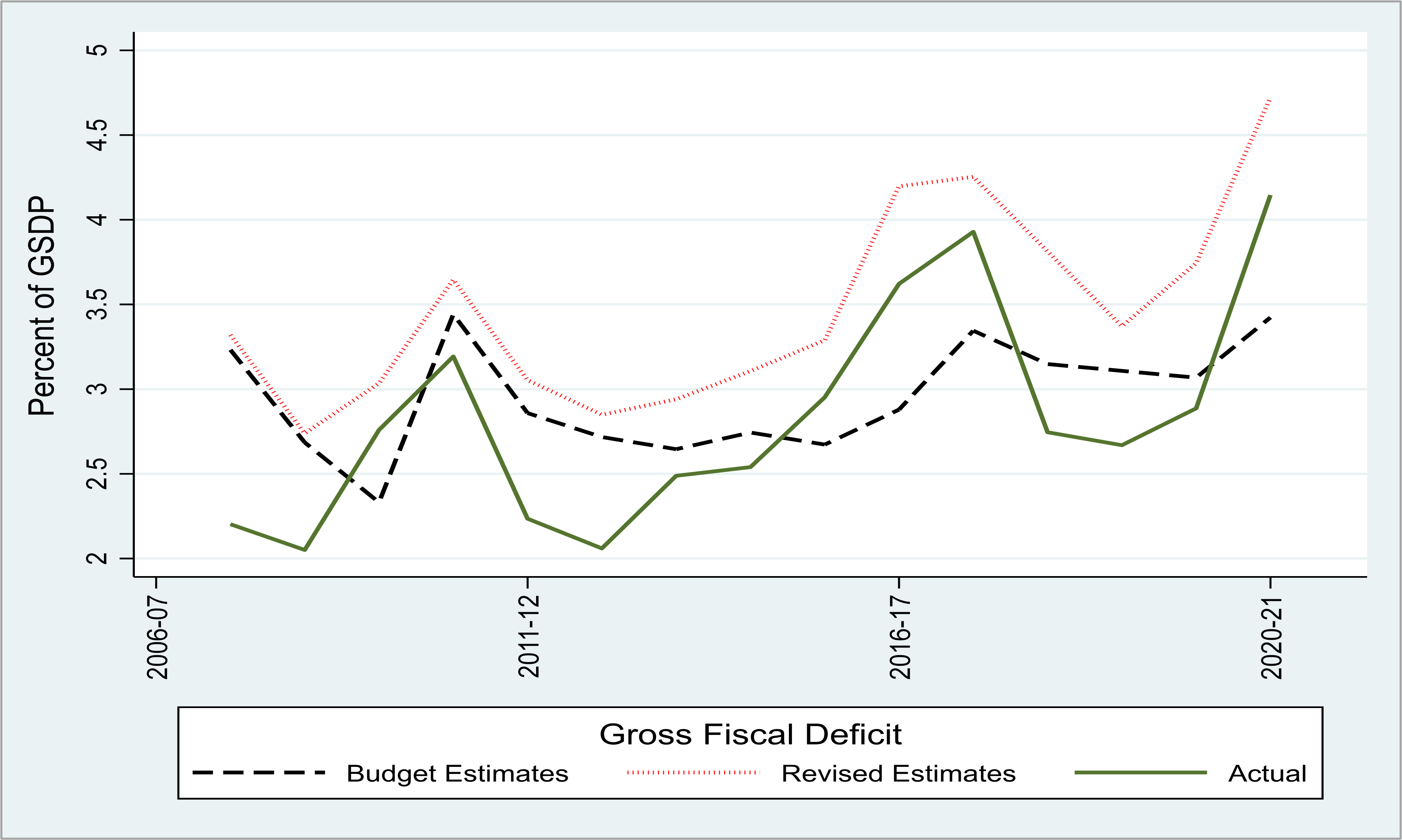

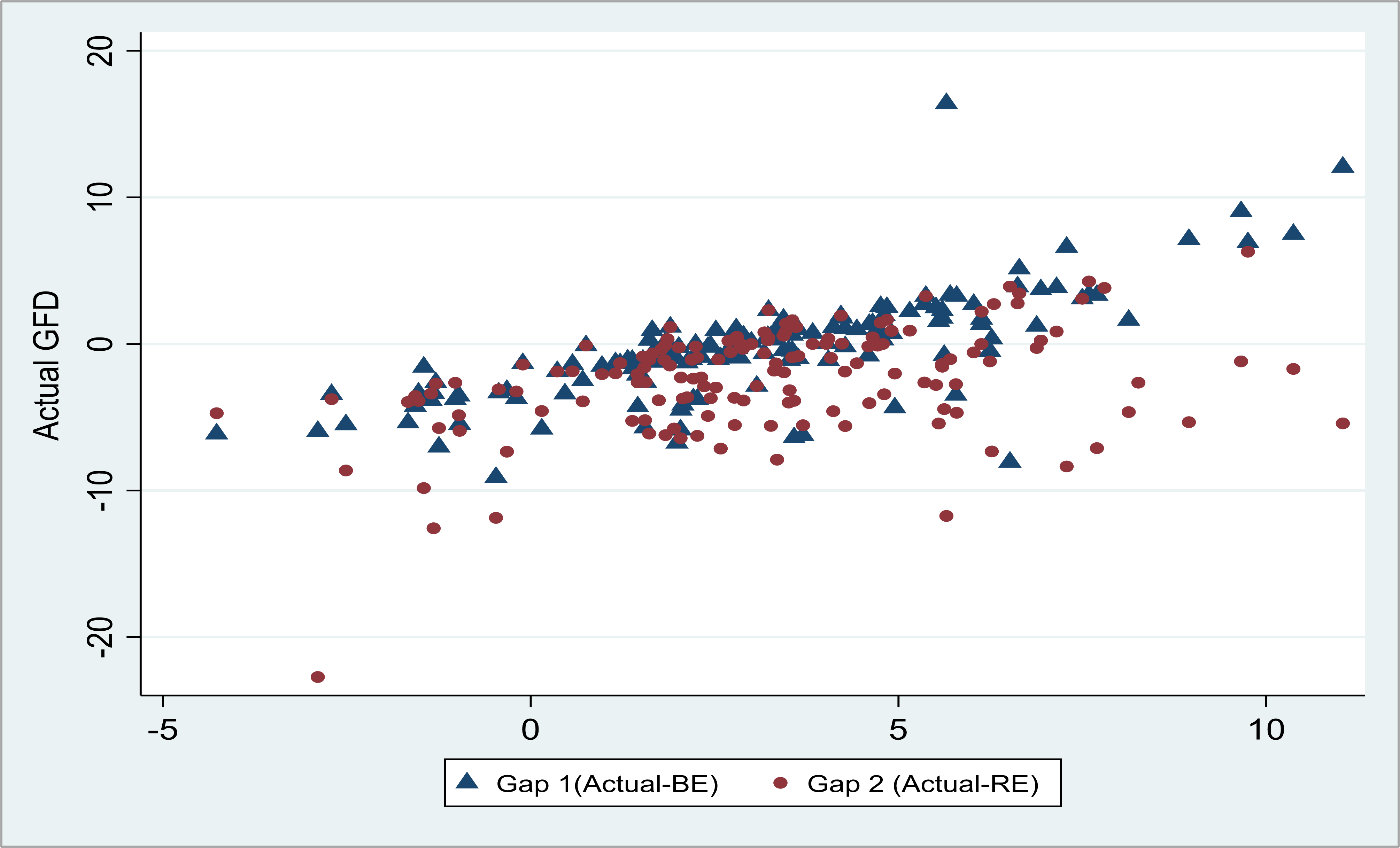

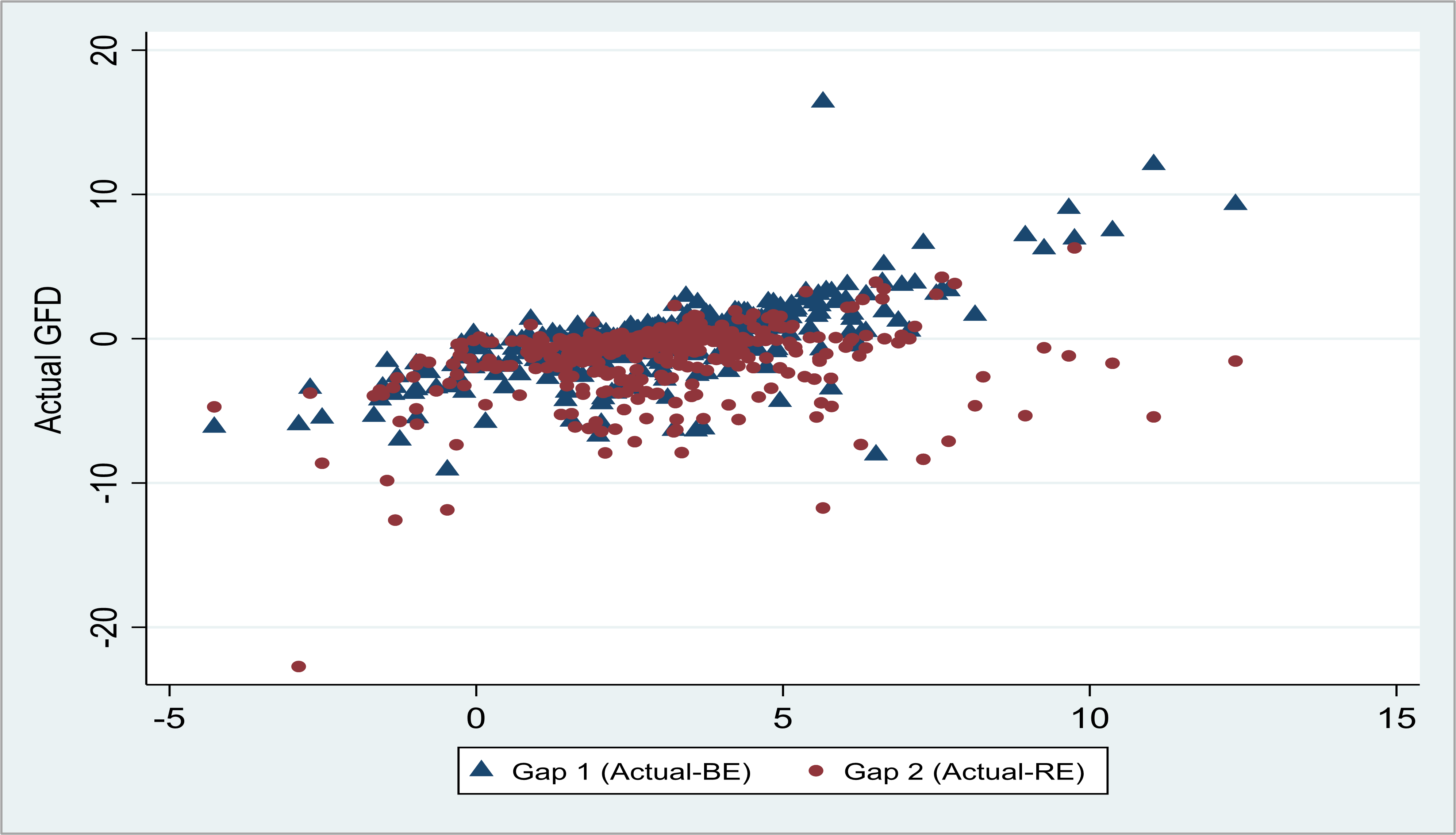

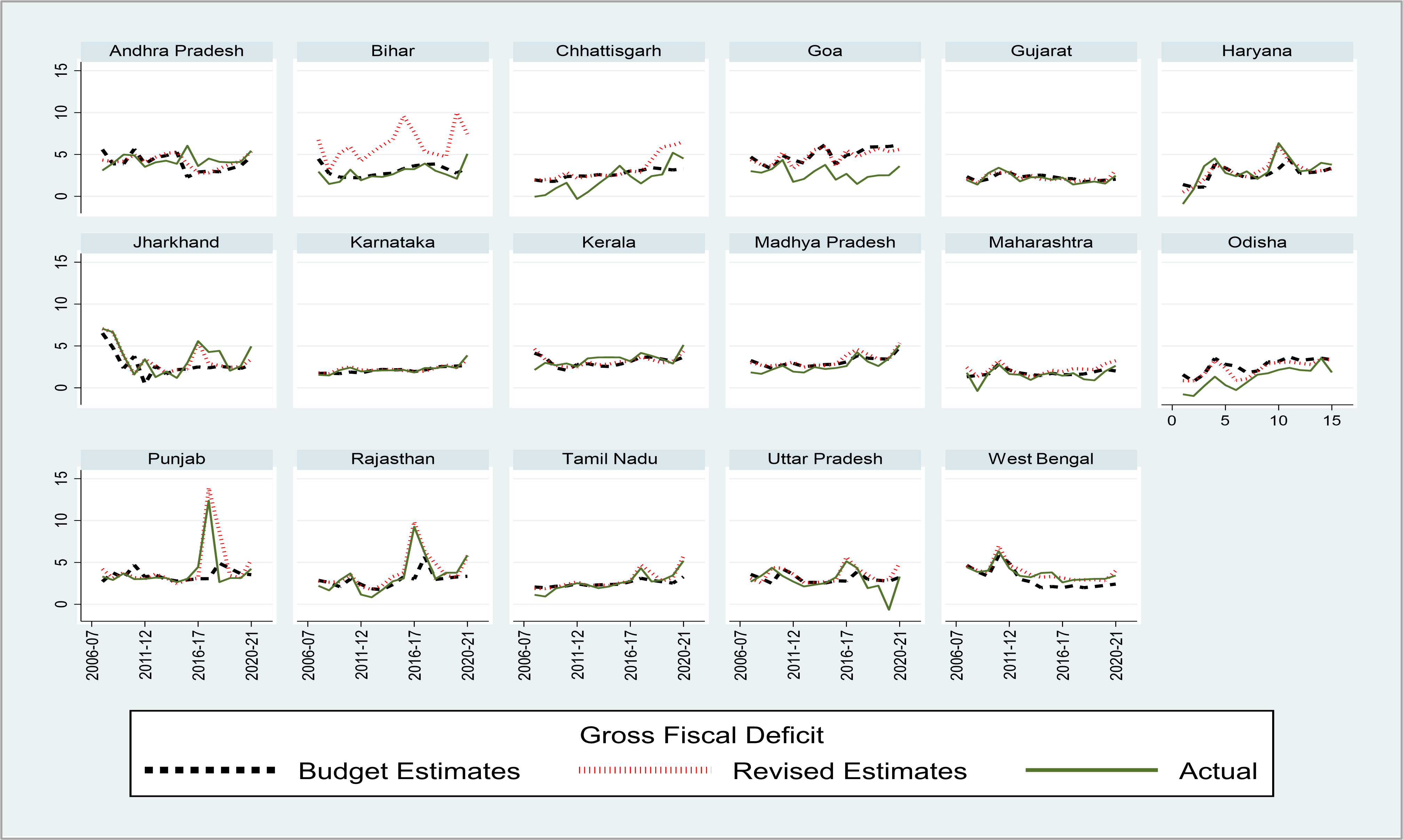

Figure 1 shows the behaviour of BE, RE, and Actual GFDs for the sample of 17 non-special states during 2006-2020. These estimates are averaged over our sample states. The RE of GFD is distinctly above the BE and Actual of GFD over our study period. The BE is between RE and Actual around the first half of our study period, and the Actual remains between RE and BE around the latter half. BE was above the Actual estimate in the first half of our sample period because the budgeted capital expenditure was not realized for most states in the first half, i.e. before 2015-16. For the significant part of the second half (after 2015-16), Actual estimates of GFD remained above BE due to an increasing focus on capital spending in recent periods where the realized amount exceeded the budgeted amount, leading to higher Actual GFD than BE. The pattern in Figure 1 is generally reflected in individual states. It is more pronounced in 11 special category states (see Appendix, Figure A4) compared to 17 non-special states (see Appendix, Figure A3). Figure 2 plots Gap1 and Gap2 (represented by the y-axis) against the actual GFD (represented by the x-axis). It shows that both the gaps increase with the actual GFD over our sample period. Gap2 (Actual-RE) scatteredness is higher than Gap1 (Actual-BE). Broadly, we observe the same patterns of Figures 1 and 2 in our sample of 11 special category states (refer to Figures A1 and A2 in the Appendix). For a better understanding, the state-wise (17 non-special and 11 special states) characteristics of RE, BE, and Actual GFDs are shown in Figures A3 and A4 of the Appendix.

__2006-2020.png)

.png)

B. Econometric Method

To examine which is a relatively better measure between BE and RE of GFD, we employ a fixed-effects panel data estimation model shown in Equation (3).[4]

Gapit=∂it+εit

where i denotes the state with and t denotes the number of years with t = The dependent variable is We construct two gaps: Gap1 and Gap2. Gap1 is the difference between the Actual/Accounts and the Budget Estimates (Actual-BE), and Gap2 is the difference between the Actual/Accounts and the Revised Estimates (Actual-RE). Therefore, denotes the considered gap in the state i in year t. is the measure of intercept in state i in year t. Note that, to test the means of these gap variables in the panel fixed-effects framework, we do not include any explanatory variables since our aim is not to study the causal determinants of the gaps. Here, we to estimate Equation (3) to investigate whether the intercept coefficient is statistically close to zero. Suppose the averages of the constructed gap variables are statistically different from zero at the standard level of significance. Then, we conclude the presence of bias (positive/negative), conditional on the signs of the coefficients.[5]

First, we execute our estimation in the sample of 17 non-special category states for 2006-2020 (17 states*15 years = 255 observations of state-year). Subsequently, we conduct a robustness test by experimenting with our main results with 11 special category states for the same period (11 states*15 years =165 observations).

IV. Empirical Analysis

The results from the 17 non-special states suggest that the average gap between Actual and BE (Gap1) is not (statistically) different from zero, suggesting that averages of Gap1 across states are almost the same. In contrast, the difference between Actual and RE (Gap2) is statistically significant, as shown in panel-a of Table 1. The negative and statistically significant sign on the coefficient of Gap2 suggests an upward bias in RE.

How do these findings behave if we consider the 11 special states in our analysis? Here, Gap1 is insignificant, and Gap2 is significant (shown in panel-b of Table 1), concurring with the findings of the sample of 17 non-special states. The only difference is that now the size of the upward bias in RE in the special category states’ sample is higher than in the sample of non-special states since the coefficient of Gap2 is now -2.27 (Panel-b) as opposed to the earlier coefficient of -0.617 (panel-a). This difference is because the GFDs of the non-special category states are better projected than the GFDs of special states.

To sum up, we can draw upon three points from our empirical analysis. There exists a bias in the RE of GFD, no matter how we define our sample (17 non-special or 11 special category states). Our finding of bias in RE concurs with the findings of RBI (2020) and RBI (2022). The bias size is more prominent in the sample of special category states than in the non-special category states. No systematic bias is involved in the BE of GFD across our samples of states.

V. Conclusions

The paper assesses two metrics, BE and RE, of GFD using data from Indian states spanning from 2006 to 2020. It uncovers a consistent bias in RE compared to BE. Consequently, policymakers and researchers can use BE as a temporary measure for macro-fiscal analysis across Indian states until actual figures are available. This recommendation stems from the observation that BE more closely mirrors the actual GFD, contrary to the common belief that RE provides a better approximation due to being based on actual data from certain months within a year.

__2006-2020.png)

.png)

__2006-2020.png)

__2006-2020.png)