I. Introduction

Since the onset of the Covid-19 pandemic, China has implemented stringent policies to restrict disease transmission, including travel limitations, testing requirements, and complete lockdowns of neighborhoods and entire cities (Kirby, 2022). The World Bank estimated that these strict zero-Covid measures reduced gross domestic product growth to 2.7 percent in 2022, the lowest rate in decades (The World Bank, 2022). While most other countries lifted their Covid restrictions in the Spring of 2022, China maintained them until November 2022, significantly impacting the economy and foreign trade (Tianlei, 2022). China’s trade data shows that exports and imports significantly declined during strict Covid measures. In 2022, exports fell by 7 percent compared to pre-pandemic levels, while imports dropped by over 10 percent, highlighting the significant trade disruptions caused by the zero-Covid policy (National Bureau of Statistics of China, 2023).

On November 11, 2022, China’s Joint Prevention and Control Mechanism Team announced the lifting of the inbound flight suspension and revised quarantine measures for incoming foreign travelers. Several Chinese cities, such as Guangzhou and Shanghai, then decided to lift their Covid restrictions despite numerous positive cases. This initiative compelled the Chinese government to abandon the zero-Covid policy, removing the requirement for negative Covid tests for daily activities and travel across regions. The policy shift resulted in a massive Covid outbreak, with some provinces reporting infection rates of almost 90 percent (Burki, 2023; Huang et al., 2023). This reversal had an immediate and measurable impact on China’s trade flows. In the first quarter following the end of the zero-Covid policy, exports fell by 9.1 percent and imports contracted by 11.5 percent. This sharp decline in trade performance correlates directly with the sudden reopening of the economy and subsequent labor shortages due to widespread infections. As restrictions eased further, trade began to recover, with exports rebounding by 13.2 percent in the second quarter, though imports remained suppressed at 7.5 percent.

Before the abrupt termination of the zero-Covid policy in China, public health researchers discussed potential opening strategies and their economic implications. Wu et al. (2023) posited that ending the Covid measures could lead to an economic recession in China, resulting in lost income, increased unemployment, and reduced economic activity. Additionally, a high infection rate among essential workers could disrupt global supply chains in China, adversely impacting the global economy (Cowling, 2023). The literature proposed a sequential opening strategy that could significantly reduce economic losses compared to a nationwide reopening and effectively suppress the peak of Covid-19 cases (Xu et al., 2023). Instead, the Chinese government opted for an abrupt end to the zero-Covid policy, causing considerable disruptions in labor markets and economic activities (May et al., 2023; Strumpf & Lin, 2022). The trade implications of this policy shift were particularly severe for labor-intensive industries such as information and communication technologies (ICT) and food processing. These sectors experienced substantial disruptions due to labor shortages resulting from the rapid rise in Covid infections. However, regions with stronger economic support during the pandemic exhibited faster recovery, particularly in exports, underscoring the varying resilience of different sectors and regions in China.

Despite extensive literature studying the global supply chain disruptions caused by Covid and the policy response (e.g., Ahn & Steinbach, 2023; Bas et al., 2023; Goldberg & Reed, 2023; Ngo & Dang, 2023), little is known about the economic implications of the end of the zero-Covid policy in China and how resilient global supply chains were to this shock. Existing research has explored the macroeconomic consequences of China’s zero-Covid policy. Gong et al. (2024) analyzed the policy’s effects on economic activities, mobility, and environmental issues, while Tang & Zheng (2024) focused on its role in subnational cross-regional export performance. Similarly, Gong et al. (2024) investigated the policy’s impact on labor market outcomes in China, highlighting the risks posed by labor shortages due to high infection rates in key sectors. However, limited research exists on the specific trade impacts following the abrupt end of the policy, which is the focus of this study.

Our paper assesses the response of international trade to the end of the zero-Covid policy in China. We rely on high-frequency trade data and counterfactual statistical methods to study the dynamic trade response. Our event study analysis reveals that China experienced an export decline of 9.1 percent and an import contraction of 11.5 percent in the first quarter after the policy shift. In the second quarter after the policy change, exports rebounded by 13.2 percent, while imports remained depressed at 7.5 percent. Our results also provide evidence of considerable heterogeneity in the trade response across trading partners, products, and Chinese provinces. Labor-intensive industries like information and communication technologies and food processing experienced a larger trade response. Interestingly, there is evidence for distinct patterns of treatment heterogeneity across Chinese regions, with those having stricter Covid policies witnessing larger trade contractions. Simultaneously, Chinese provinces that received substantial economic support during the Covid pandemic saw a more robust trade recovery in the second quarter following the end of the zero-Covid policy. Our findings underscore the considerable trade disruptions caused by the policy shift and highlight the resilience of international trade in the face of global market disruptions due to the end of zero-Covid in China.

II. Data and Methodology

We rely on an event study framework to evaluate the dynamic effects of the termination of China’s zero-Covid policy on foreign trade. Event studies have been commonly employed to examine ex-post treatment dynamics (e.g., Ahn & Steinbach, 2023; Carter et al., 2022; Steinbach, 2022). Leads and lags relative to the event of interest are included to capture pre-trends and assess the post-event treatment dynamics, as described by Freyaldenhoven et al., 2021. A non-linear panel regression model is used to evaluate the treatment dynamics of China’s foreign trade:

Xij, t=exp(αij,yr +αij,mo+5∑m=−3βmrij,t−m)+ηij,t

where denotes the Chinese province, the foreign trading partner, and the month. The outcome of interest is denoted with and maps into the export and import values. We assume that the high-dimensional fixed effects at the province-country-event-year and province-country-event-month levels account for all latent confounders. Among others, potential confounders captured are level differences in the trade outcome and seasonality patterns. The event study is centered around November 2022, when the Chinese government announced the sudden ending of the zero-Covid policy. We measure the dynamic trade response three months before and five months after the event with the term: We follow earlier work by Carter et al. (2022) and Steinbach (2023) and use trade flows from 2015 to 2018 to construct a control group unaffected by the policy shift. This approach allows us to account for the cyclic nature of trade flows and obtain a reliable counterfactual for causal inference.

Following standard practice in the related trade literature, we rely on the Poisson pseudo-maximum likelihood estimator to identify the parameters of interest and account for the high-dimensional fixed effects with an iteratively re-weighted least-squares algorithm (Correia et al., 2020; G. Gong & Samaniego, 1981; Silva & Tenreyro, 2006). Because we suspect the standard errors to be correlated at the province-country level, we cluster them this way (Cameron & Miller, 2015). We compiled monthly trade data at the province-country-pair level from the General Administration of Customs of China (2023). The final balanced dataset covers 6,745 province-country pairs at the 2-digit Harmonized System level from January 2010 to April 2023. We used this data to construct the event study panel, which is centered around November 2022. Descriptive statistics are provided in Table A of the Appendix. We aggregate the trade data at the province-country level for the main analysis and use chapter-level trade flows to analyze heterogeneity in the treatment effects according to product characteristics.

III. Results

A. Baseline results

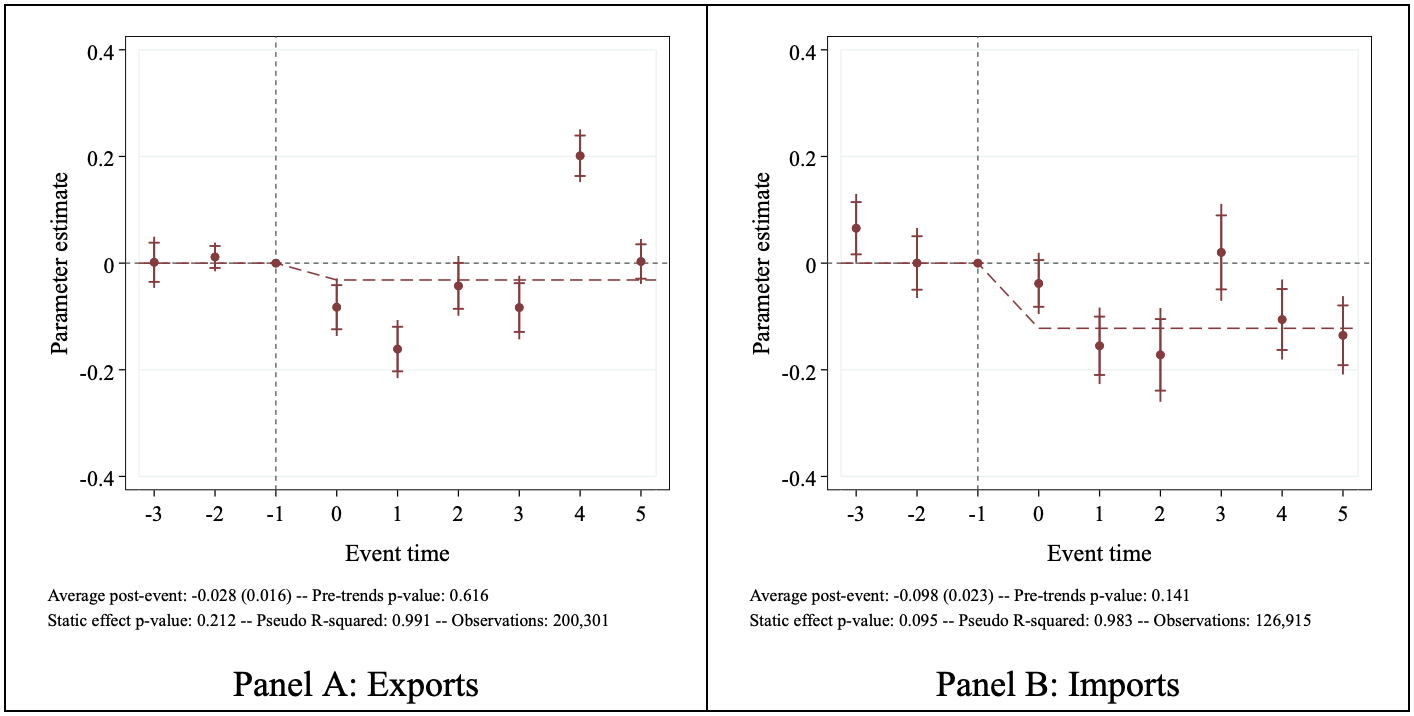

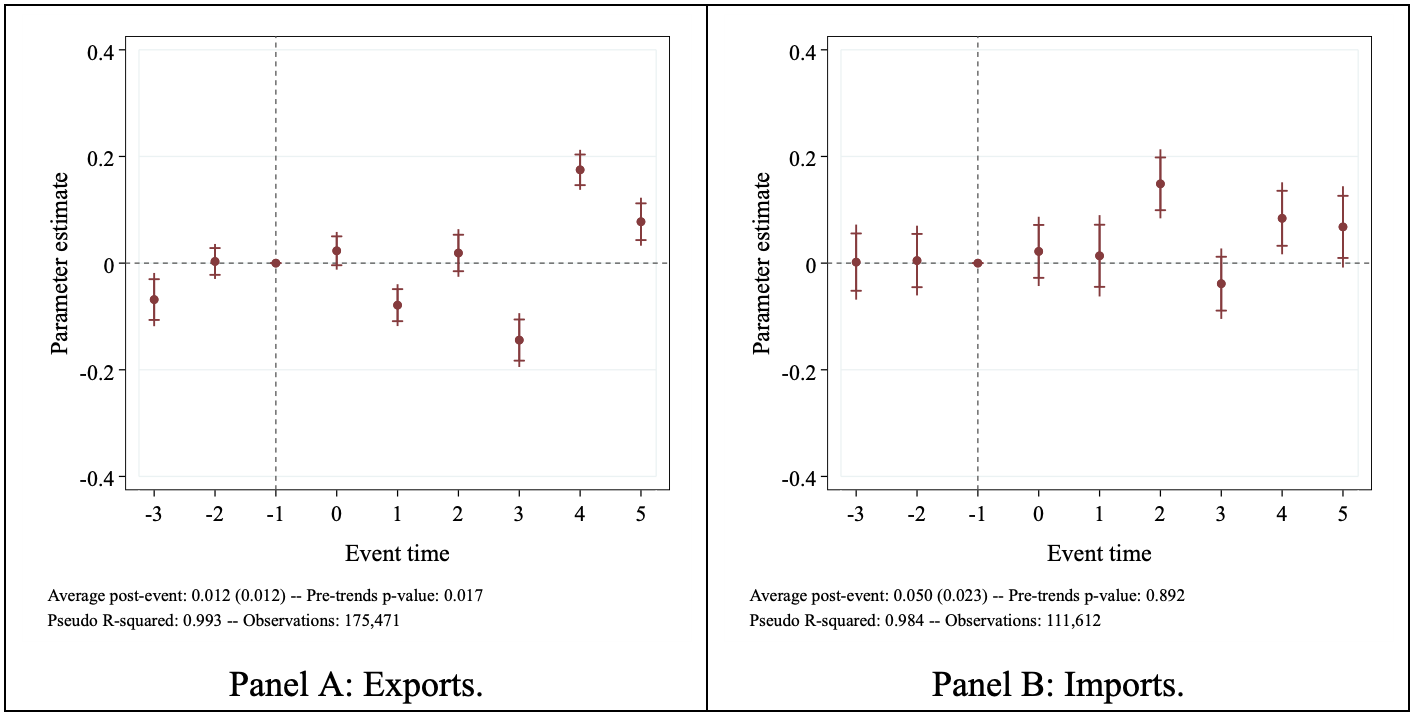

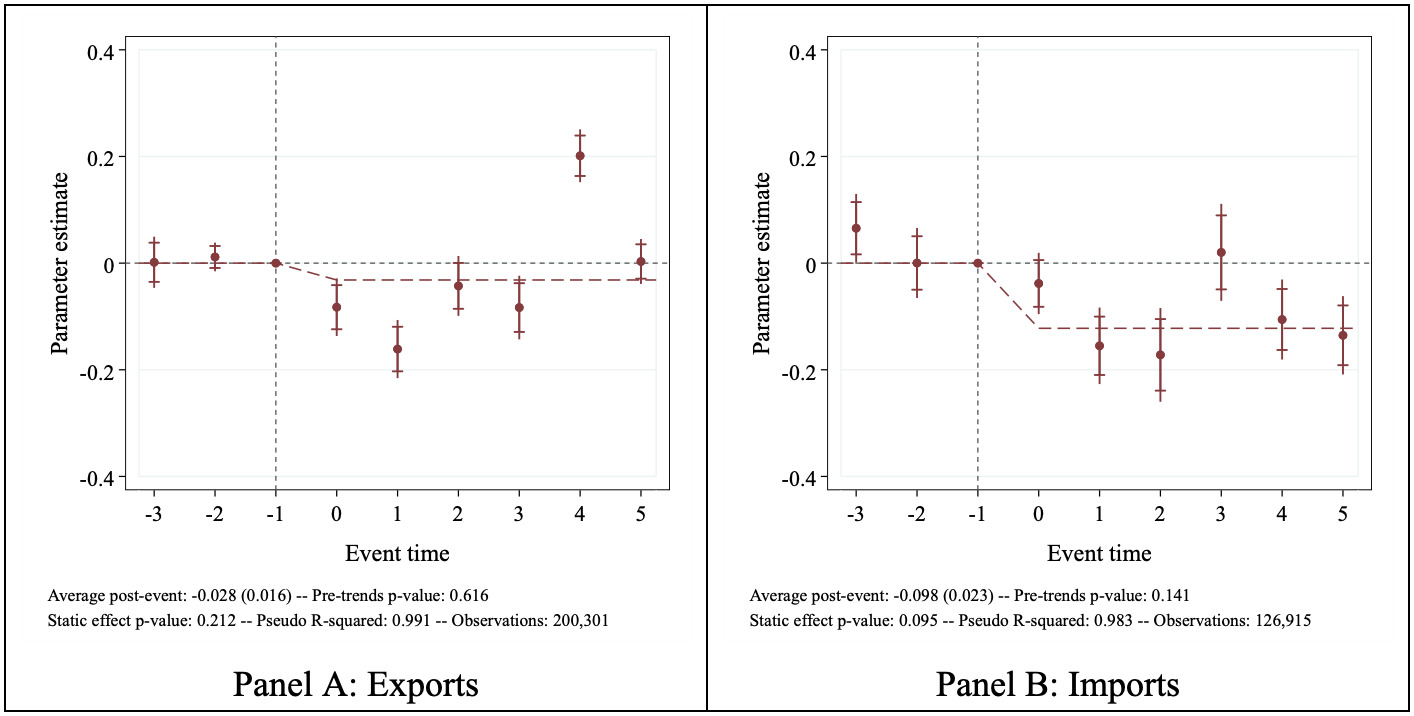

Figure 1 presents event studies analyzing the impact of the conclusion of China’s zero-Covid policy on its foreign trade. Panels A and B display dynamic treatment estimates, 95 percent confidence intervals, and uniform sup-t bands following Montiel Olea and Plagborg-Møller (2019). Additionally, we include static regression model estimates indicated by dashed red lines. Panels A and B also report Wald test statistics for pre-trends and the static effect p-values.

The analysis indicates no significant pre-trends for either outcome, suggesting that the treatment group exhibited trends similar to the control groups during the pre-treatment period when high-dimensional fixed effects were considered, thereby validating the research design (Freyaldenhoven et al., 2019; Sun & Abraham, 2021). In the first quarter following the end of the zero-Covid policy, exports decreased by 9.1 percent, and imports declined by 11.5 percent relative to the counterfactual level.

In the second quarter post-treatment, China’s exports demonstrated a recovery with a 13.2 percent increase, whereas imports remained significantly lower at approximately 7.5 percent. These findings suggest that exporting firms quickly adjusted to the economic disruptions caused by the termination of the zero-Covid policy, while the recovery in imports lagged.

B. Robustness checks

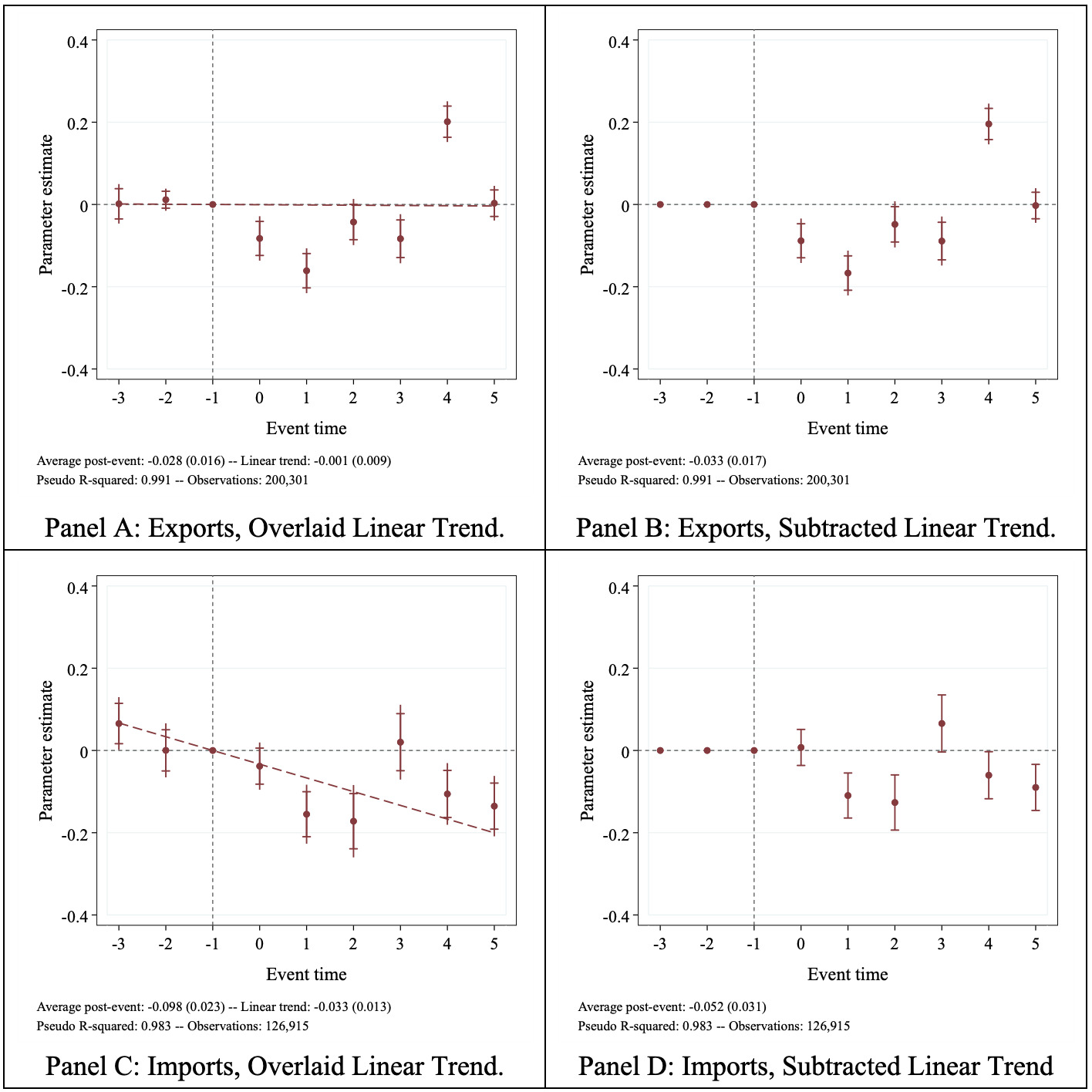

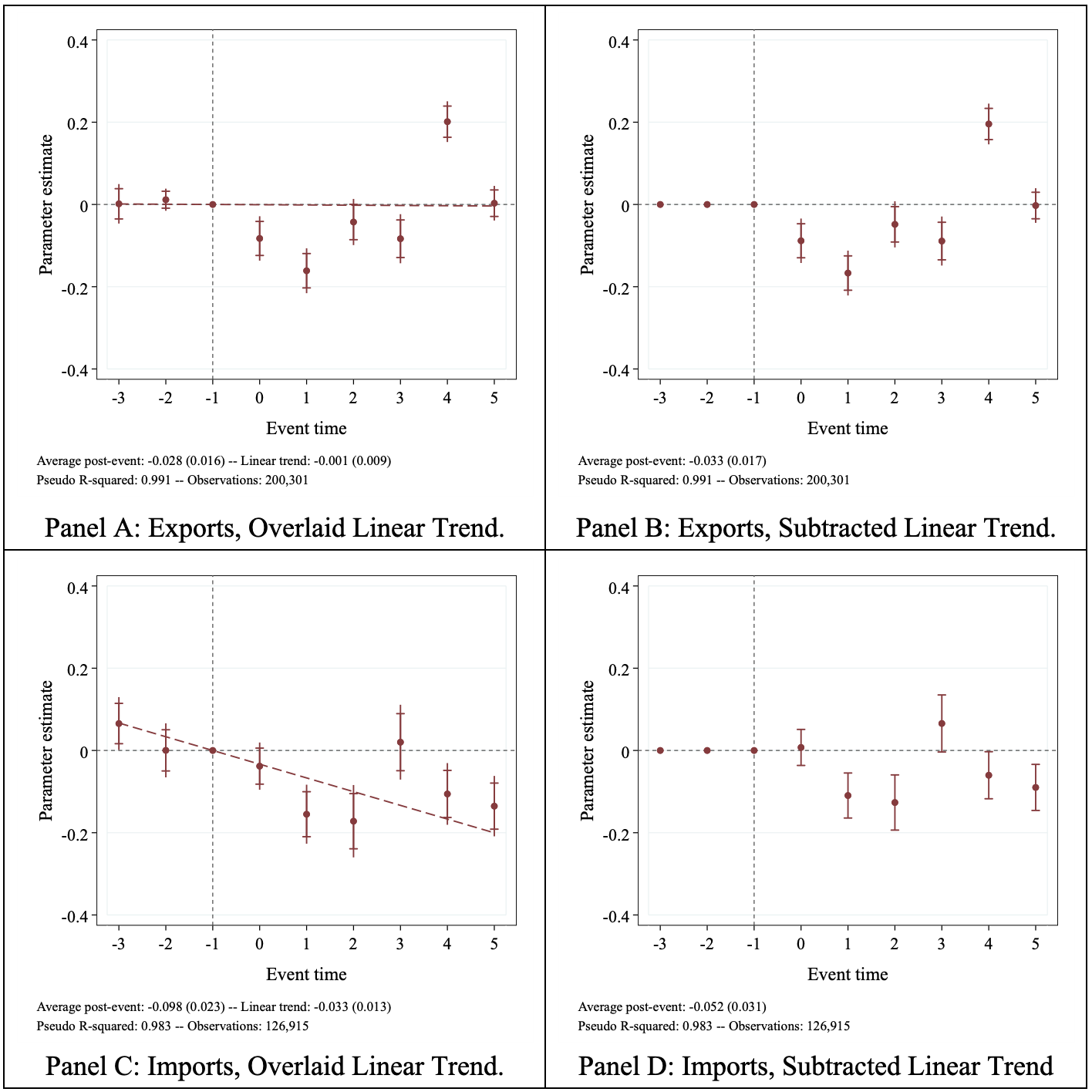

We conducted four robustness checks to ensure the validity of our main results. First, we estimated Equation 1 under an alternative set of fixed effects that absorb less variation in our data. The results of this exercise are shown in the Appendix (see Table B) and indicate no statistically significant differences in the average post-event treatment effects. Second, we compared the estimated treatment effects for three alternative control groups in the Appendix (see Table C). Again, we found limited statistical evidence for significant differences in the estimated dynamic treatment paths. Third, we estimated a placebo model, assigning the treatment to November 2010, which we presented in the Appendix (see Figure A). We found no evidence of a statistically significant relationship between the outcomes and treatment. Lastly, we estimated Equation 1 under the alternative assumption that the treated units would have continued their pre-event paths. We applied the method established by Dobkin et al. (2018) and fitted a deterministic linear trend in event time with a unit-specific slope. We overlaid the estimated linear pre-trends in Panels A and C and presented post-event treatment paths with subtracted linear pre-trends in Panels B and D of Figure B (refer to Appendix). After accounting for linear pre-trends, the estimated average post-treatment effect shifted from a 2.8 percent decrease to a 3.2 percent contraction for exports and from a 9.3 percent drop to a 5.1 percent reduction for imports. It is important to note that the estimates for exports do not differ significantly from each other at conventional levels of statistical significance.

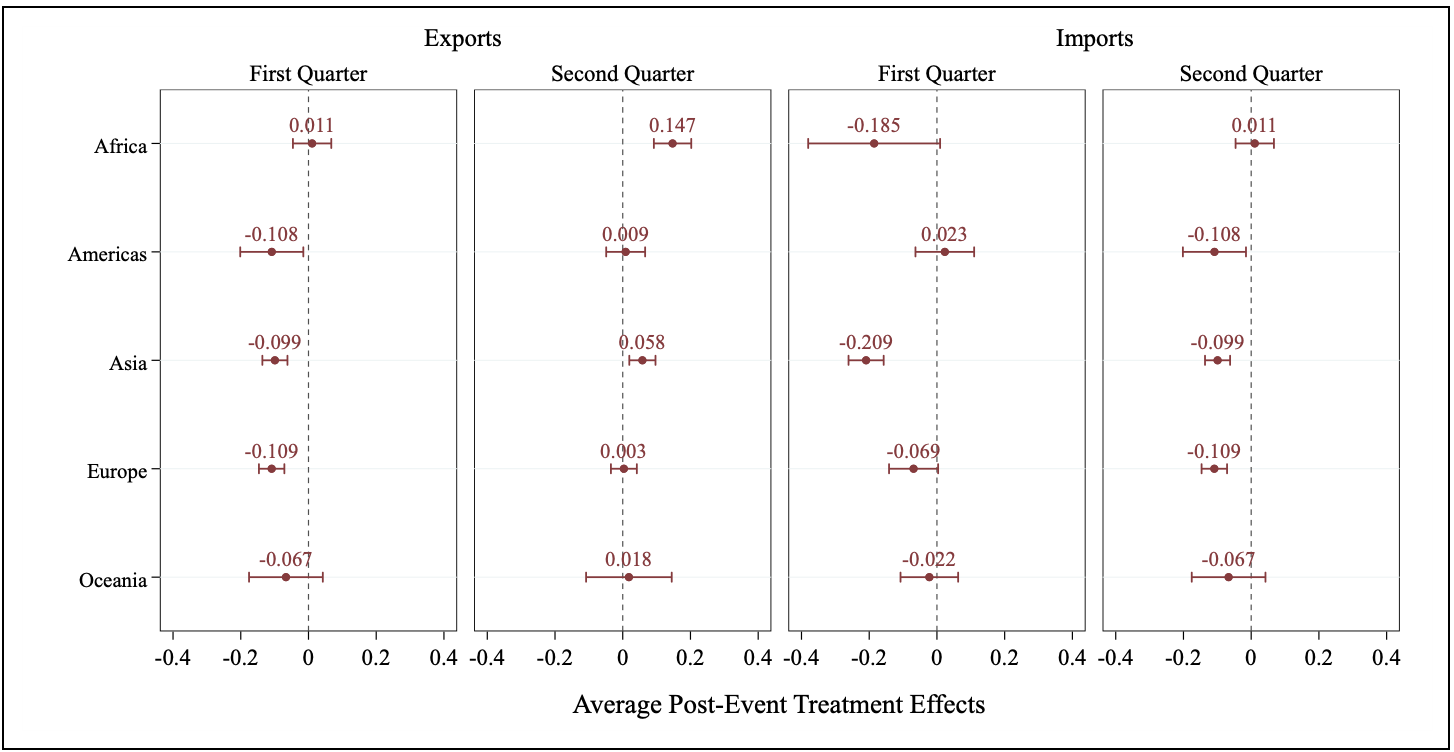

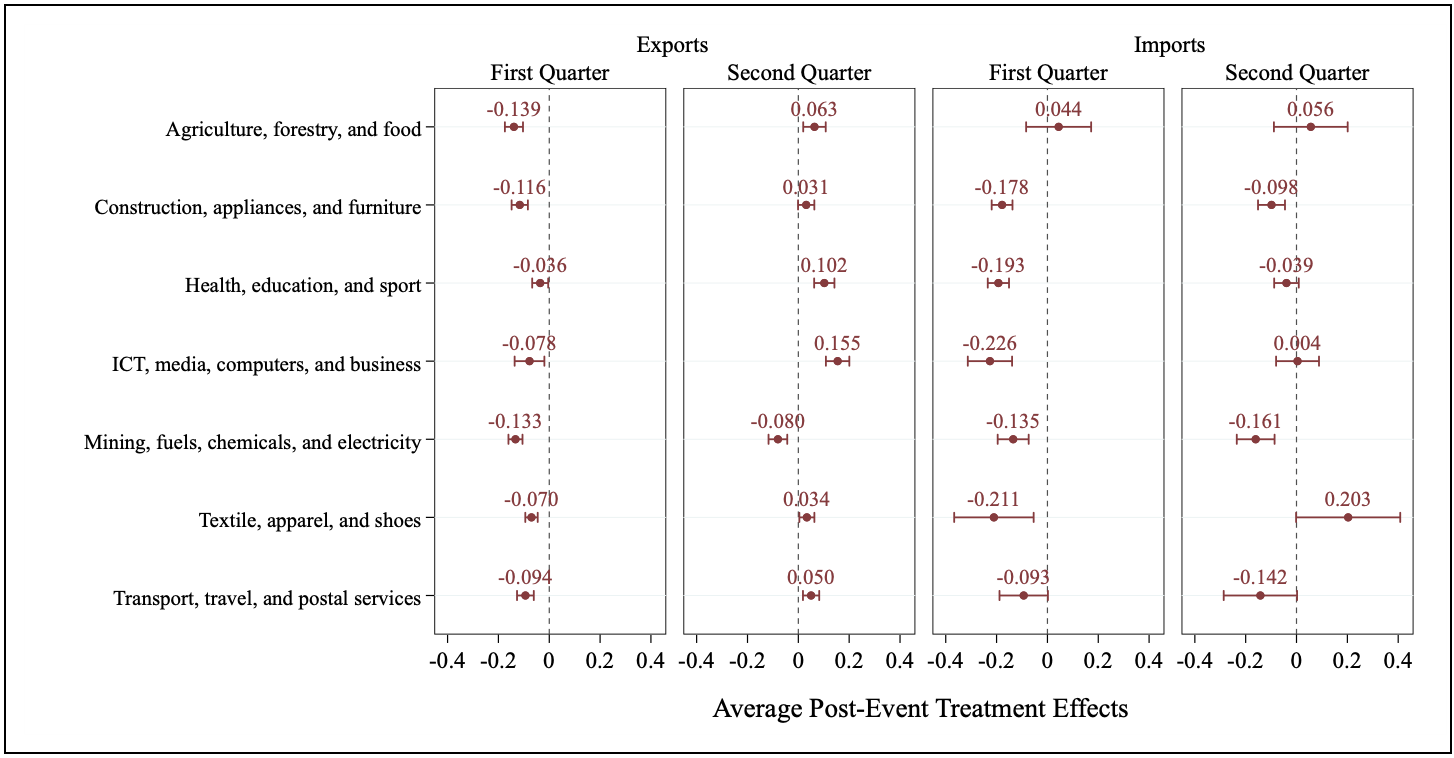

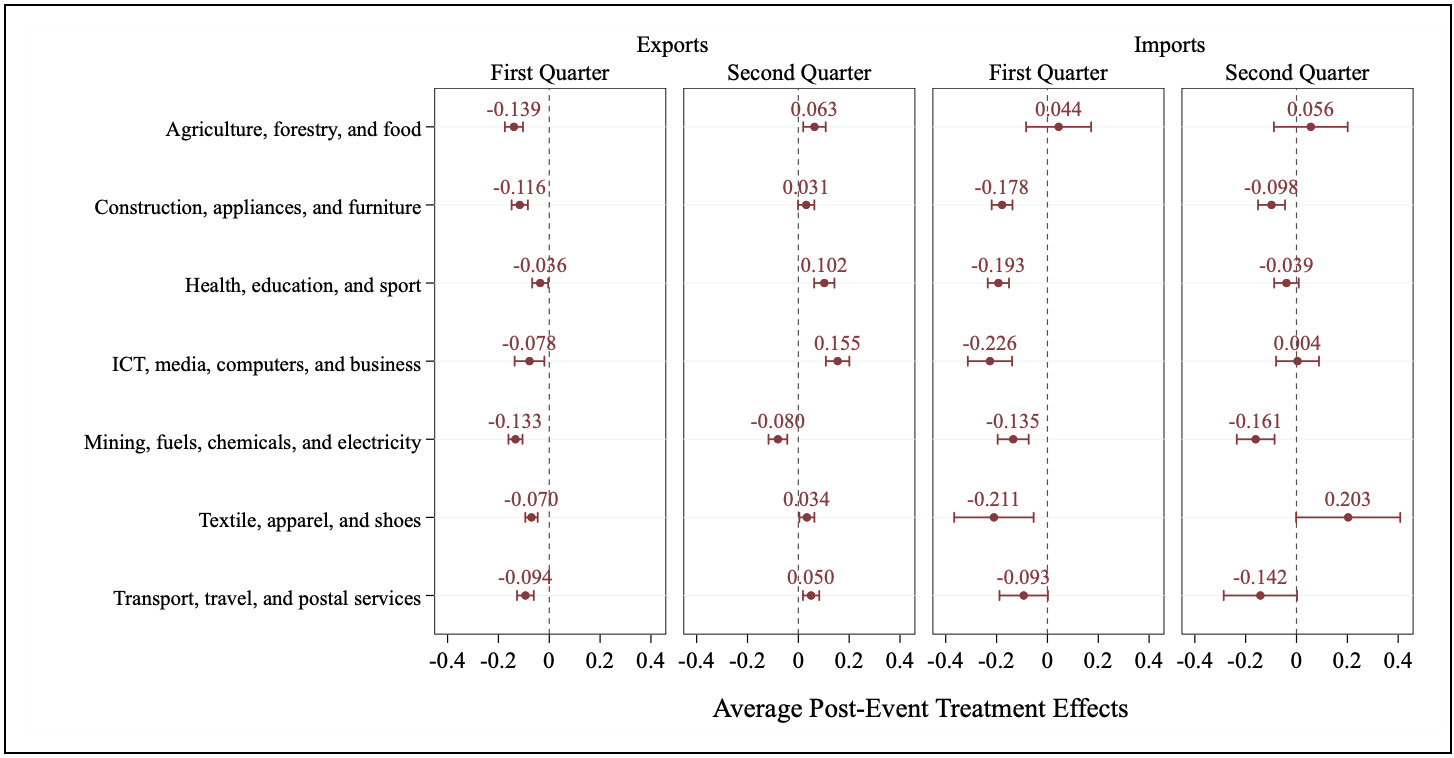

To better understand the mechanisms underlying the observed differences in the post-event treatment paths, we investigated treatment heterogeneity according to the trading partner, product group, and characteristics of Chinese provinces. First, we show estimates by geographic region in Figure 2. The average post-event treatment effects reveal that the initial export shock was similar across export destinations. Interestingly, the recovery was more robust for export destinations in Africa and Asia. In contrast, there is considerable heterogeneity in the import response, with imports from Asian trading partners contracting by 18.9 percent, while those from the Americas were unaffected in the first quarter after the end of the zero-Covid policy. Figure 3 shows that the initial trade shock affected all industries, with agriculture, forestry, and food exports contracting the most, while the recovery was more robust for the information and communication technologies (ICT) industry. In contrast, the evidence for import recovery is much weaker, with mining and fuel imports remaining the most depressed at 14.8 percent in the second quarter. At the same time, textile imports from other Asian countries rebounded strongly, reaching about 22.6 percent above the counterfactual level in the second quarter after the end of the zero-Covid policy. Notably, imports from the Americas were 10.3 percent below the counterfactual in the second quarter after treatment, speaking of the delayed response in shipment cancellation from those countries. Second, we reveal considerable heterogeneity in the trade response according to industry characteristics.

We now turn to heterogeneity in the trade response according to province characteristics in Table 1. Panel A shows that Chinese provinces that implemented stricter Covid policies saw a more considerable reduction in exports in the first quarter after the end of the zero-Covid policy. At the same time, there is little evidence for treatment heterogeneity in the import response. A similar pattern exists for provinces with a free trade zone, as shown in Panel B. Exports from those contracted by 10.2 percent, while they expanded above the counterfactual level in provinces without a free trade zone. Again, there is little evidence of treatment heterogeneity in the import response. Panel C corroborates these findings, indicating that more populated areas saw a more substantial initial export decline and a weaker recovery in the second quarter after the zero-Covid policy. Lastly, looking at the economic support received by the Chinese provinces during the Covid pandemic, we find that exports from those provinces with the strongest economic backing contracted by about 11.7 percent but recovered faster than those from other provinces. Again, there is little evidence for treatment heterogeneity on the import side.

IV. Conclusion

This paper examines the trade response to the end of the zero-Covid policy in China, utilizing high-frequency trade data, counterfactual statistical techniques, and event study methods. Following the end of the Covid restrictions, China experienced a significant contraction in foreign trade, with exports declining by 9.1 percent and imports dropping by 11.5 percent below the counterfactual level in the first quarter after the policy shift. Notably, the trade recovery was stronger for exports compared to imports. In the second quarter after the policy change, China’s exports rebounded by 13.2 percent, while imports remained depressed at 7.5 percent. Our heterogeneity analysis revealed distinct patterns of treatment variation across export destinations and industries. For instance, labor-intensive industries, such as ICT and food processing, experienced larger adverse trade effects. Interestingly, Chinese provinces exhibit distinct patterns of treatment heterogeneity, as provinces with stricter Covid policies witnessed larger trade contractions. Concurrently, those provinces that received substantial economic support during the Covid pandemic saw a more robust export recovery in the second quarter following the end of the zero-Covid policy. These findings underscore the significance of trade disruptions caused by the policy shift and highlight the resilience of international trade in the face of market disruptions resulting from the end of zero-Covid in China.

To mitigate trade disruptions caused by abrupt policy changes like the end of the zero-Covid policy, a phased reopening with targeted support for labor-intensive sectors could have reduced supply chain shocks. Strong institutional frameworks, including effective legal enforcement, play a key role in ensuring business continuity. Governance, transparency, and adherence to the rule of law are essential in fostering resilience in international trade, particularly during crises. Additional research is required to identify the policy measures that could improve global supply chain resilience.