I. Introduction

During the first quarter of the 21st century, emerging economies have witnessed crucial structural transformation. Starting from the liberalization of the financial sector to becoming major players in the markets, emerging economies have achieved remarkable progress. For instance, they account for 45% of the global GDP (Global Economic Prospects, 2025) and have attained higher economic growth, even when advanced economies were not performing well. Apparently, the performance of emerging economies in the early 2000s and through the global financial crisis (GFC) in 2008-09 sparked a vigorous debate called ‘Decoupled or Decoupling’ on whether EMEs’ growth performance is independent of advanced economies.

It is evident that India and China were not significantly affected by the weaker growth of advanced economies and the global recession (Artis et al., 2011). However, although some EMEs experienced negative growth in 2008-09 due to exposure to the GFC, they quickly bounced back to their previous growth trajectory. This supports the belief that emerging economies have reduced dependence on advanced economies (Willett et al., 2011). These observations strengthen the decoupling argument and suggest that emerging economies are no longer strongly linked with advanced economies’ business cycles. Hence, this raises the question of whether emerging economies have decoupled from their advanced counterparts.

Empirical literature provides strong support for the decoupling hypothesis (see Akın & Kose, 2008; Kose et al., 2012). Further, Genc et al. (2010) affirmed the decoupling of GCC economies from the US, while Nachane and Dubey (2013) provide strong evidence in favor of decoupling. Similarly, Fidrmuc and Korhonen (2010) found that the pattern of Asian emerging economies exhibits low synchronization with OECD economies, while Dooley and Hutchison (2009) confirm that emerging economies decoupled from the US financial market from early 2007 to summer 2008. In a similar context, Pesce (2014) affirmed growing resilience in emerging economies, which strongly supports the decoupling hypothesis.

On the other hand, He and Liao (2012) affirmed that Asian economies cannot decouple completely, although they maintain a strong independent cycle among themselves. In sharp contrast, Lam and Yetman (2013) confirmed decoupling as a fairytale rather than a fact or forecast. Similarly, Herrerias and Ordonez (2014) found the relevance of the US cycle during the recession and rejected the decoupling hypothesis. In this context, Kim et al. (2011) found that East Asian economies became more recoupled with the G7, which rejects decoupling. Similarly, Walti (2012) found that the interdependence of the business cycle becomes stronger, strongly rejecting decoupling. Overall, the literature presents inconclusive evidence on decoupling.

With this background, we explore the decoupling hypothesis for India. We choose India because (1) it is one of the fastest growing emerging economies, (2) one of the three largest emerging economies (called EM3), and (3) given the increasing trade and financial linkages, it is crucial to verify the influence of the performance of advanced economies on the Indian business cycle and to build a shield against exposure to external shocks.

Our approach to examining the decoupling hypothesis is as follows. First, we chose the G7 as a reference economy and collected GDP data for 1996Q2–2024Q3. Studying decoupling with the G7 is crucial to analyze India’s dependence on major advanced economies whose performance greatly influences global trade and financial flows. Furthermore, whether India can achieve an independent growth trajectory if advanced economies witness slower demand is of great policy importance. Second, we adopt the Baxter-King filter to retrieve the business cycle and perform correlation analysis. Third, we construct the Euclidean distance-based decoupling index developed by Walti (2012). Fourth, we examine the existence of structural breaks to test the decoupling hypothesis using the ordinary least squares (OLS) method. Finally, we perform a comparative analysis with respect to the GFC. The empirical findings reveal: (1) evidence of incomplete decoupling, (2) India cannot be completely decoupled from the G7, (3) India shows strong coupling with Canada and the US, (4) the decoupling hypothesis is rejected except for Italy, and (5) decoupling has increased in the aftermath of the GFC. Overall, the increasing decoupling with the G7 could be due to effective domestic policies, stronger domestic demand, higher contribution from the service sector, and trade diversification.

This paper makes two contributions to the literature. First, as far as we know, this is the first study to explore the decoupling hypothesis for the Indian context using multiple decoupling methods. Second, we applied the Euclidean distance-based decoupling method, which allows us to track the degree of interdependence and visually identify structural breaks. Overall, we add to the existing decoupling literature.

The paper is structured as follows. Section II covers the data and methodology. Section III presents empirical findings. Finally, Section IV provides the conclusion.

II. Data and Methodology

We utilized quarterly data from 1996Q2 to 2024Q3. We collected gross domestic product data for India and the G7 from the CEIC database. We used ISO codes such as CAN, FRA, DEU, ITA, JPN, UK, and US for the respective G7 countries. We retrieved the business cycle using the Baxter and King (1999) filter, which applies both high-pass and low-pass filters to eliminate high-frequency noise. Only the cyclical components of a series are retained after the band-pass filter removes high-frequency fluctuations (less than six quarters) and long-term trends (more than thirty-two quarters). As a result, the extracted cyclical component is free from fluctuations caused by high or low frequencies. We then estimated the correlation coefficient, which measures the degree of association between two business cycles. A positive (negative) correlation indicates recoupling (decoupling), while perfect decoupling is established when the correlation is zero.

We constructed the decoupling index proposed by Walti (2012), which measures interdependence based on the Euclidean distance between two standardized business cycles. This index is advantageous because it provides information similar to correlation and enables structural break testing. Furthermore, this index can be plotted as a graph, allowing us to visually observe whether the Euclidean distance has increased over time. The index of interdependence between two business cycles can be constructed as follows:

∅E,A(t)=|CycleE(t)−CycleA(t)|

Here, and are the business cycles of emerging and advanced countries, respectively, while represents the time. where the business cycles are perfectly the same. The positive value indicates imperfect synchronization, and a higher distance indicates less dependency and higher decoupling.

Another way to test decoupling is to regress the dependent cycle on the reference cycle with a dummy interaction term, capturing the value within the sample period. If the slope coefficient remains unchanged, its value should be zero. The model takes the following form:

CycleIndiat=α+βCycleG7t+γCycleG7t∗Dt+εt

Here, and is the business cycle of India and G7, respectively, while represents the period. is the dummy interaction term included to test the structural break in interdependence. If the coefficient is negative and significant, the decoupling hypothesis holds; otherwise, it is rejected. The coefficients are estimated using ordinary least squares (OLS). For the dates of structural breaks, we introduced the period 2007Q4–2009Q2, as per recession dating, which strongly aligns with the GFC period. This inclusion is crucial to identifying whether the Indian economy decoupled from the G7 during the GFC.

III. Empirical Findings

The correlation coefficient between India and the G7 economies is positive, except for Italy, which indicates a positive association and rejects the notion of perfect decoupling. Furthermore, India’s business cycle is highly correlated with those of the United States and Canada. The correlation coefficients are presented in Table 1.

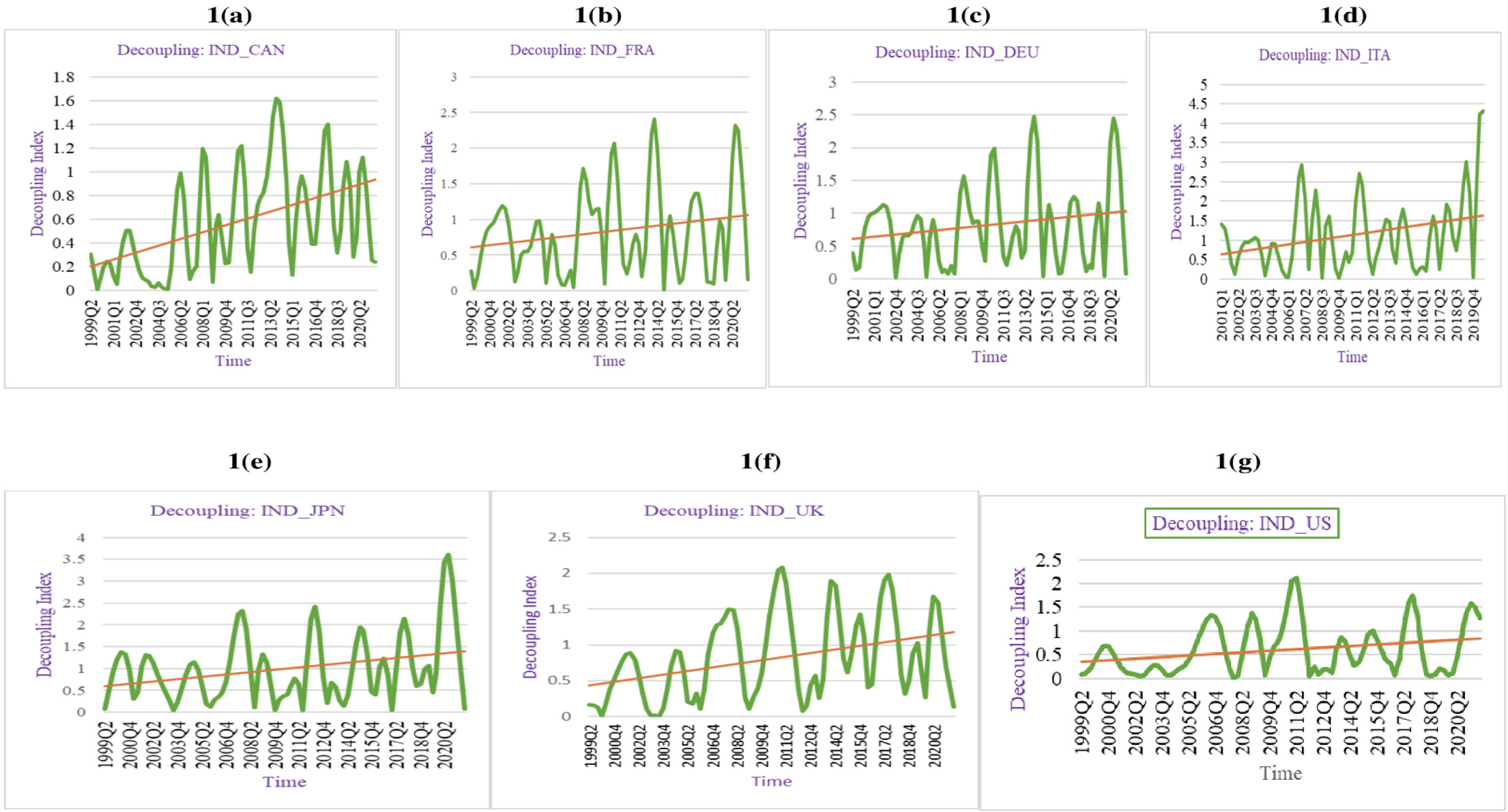

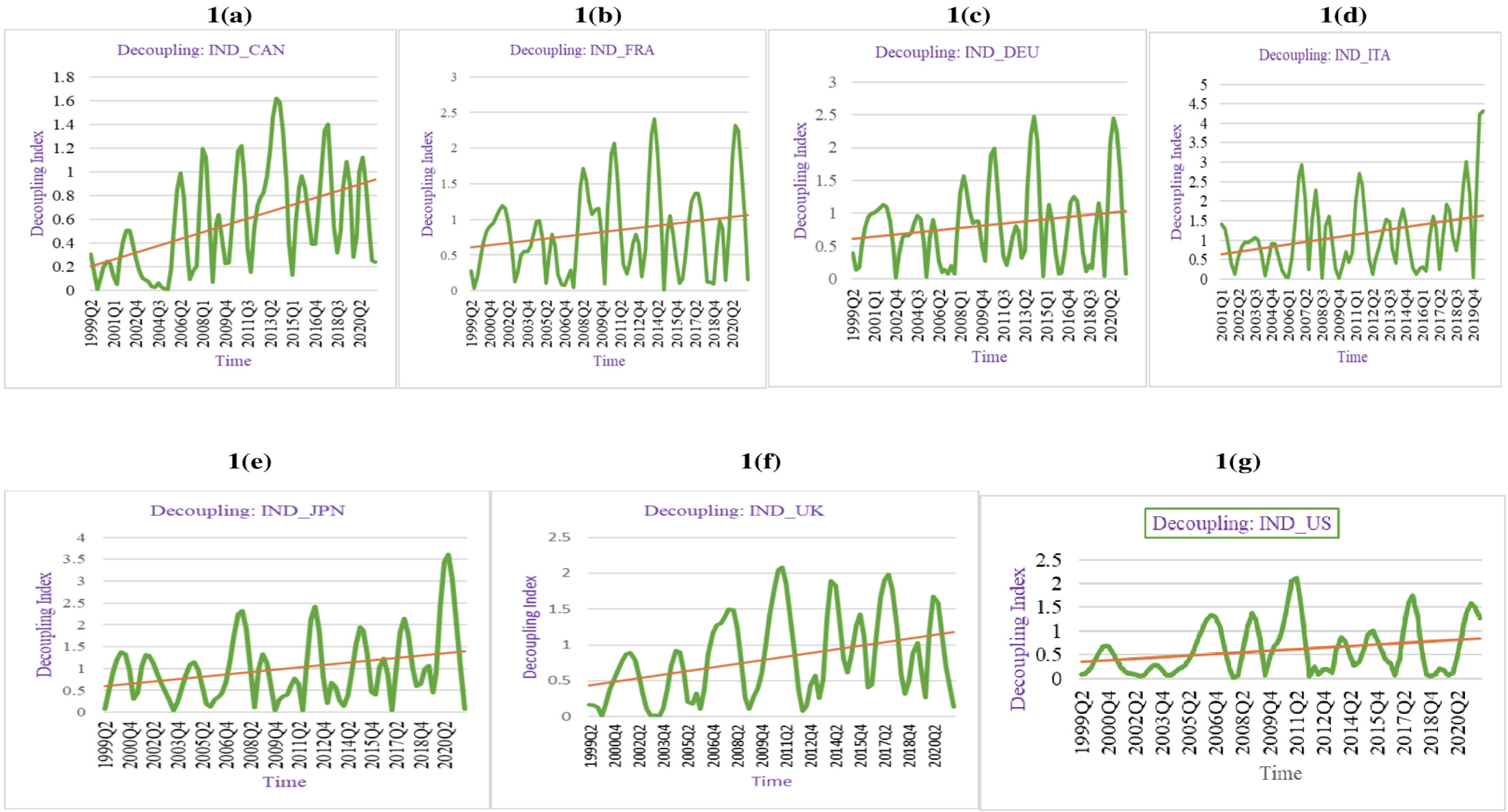

The decoupling index based on Euclidean distance is graphically represented in Figure 1. It shows that decoupling has increased over time. In most cases, the index remains within a bound (0–2.5), indicating the presence of decoupling. The Indian business cycle has experienced the greatest decoupling with Italy, while decoupling with Japan has risen since 2018. Furthermore, consistent with the correlation coefficient findings, the Indian business cycle is less decoupled from those of Canada and the US. This demonstrates their relevance to the Indian business cycle. Overall, complete decoupling is rejected, indicating only partial decoupling. Additionally, decoupling has risen over time. This finding aligns with He and Liao (2012), who state that Asian economies cannot be fully decoupled from advanced economies.

The decoupling values are reported in Table 2. The average decoupling indicates that the business cycles of Canada and the US have the lowest values, highlighting their relevance to the Indian economy. Conversely, the Indian business cycle has experienced the highest level of decoupling with the Italian business cycle. Overall, it is evident that decoupling has increased in the aftermath of the GFC, supporting the observation that decoupling is on the rise.

The findings from the structural break analysis are presented in Table 3. We do not find any evidence supporting the decoupling hypothesis during the GFC. The 𝛾 coefficient is positive and insignificant for India’s cyclical pairings, except for Japan and Italy. Although the pairing with Japan shows a negative coefficient, it is also insignificant. The only country that confirms the decoupling hypothesis with the Indian business cycle is Italy. Overall, India has not decoupled from the G7, except with Italy during the GFC. This result is consistent with Herrerias and Ordonez (2014), who highlight the relevance of the US cycle during the recession. Furthermore, the 𝛽 coefficient values are positive and significant for all pairs except Italy, indicating their relevance to the Indian business cycle. In conclusion, India cannot be completely decoupled from the G7.

IV. Conclusion

This study examines the decoupling hypothesis in the Indian context. The findings reveal incomplete decoupling, suggesting that India cannot completely decouple from advanced economies. The decoupling hypothesis is strongly rejected except in the case of Italy, which highlights the dominance of the US business cycle during the recession. Furthermore, India demonstrates strong coupling with Canada and the US. Overall, there has been a rise in decoupling in the aftermath of the GFC. This suggests that while India should monitor the US business cycle when formulating stabilization policies, economic ties with Italy may offer greater advantages. Additionally, these findings provide valuable insights into portfolio diversification.

This study opens new avenues for future research, particularly for emerging economies interested in studying decoupling. Moreover, the concept that decoupling from advanced economies could lead to recoupling with others presents an interesting area for further exploration.

Credit Author Statement

Rakesh Padhan: Conceptualization, Methodology, Software, Validation, Investigation, Writing.