I. Introduction

The volume of credit to the private sector by financial institutions has experienced a sharp increase in China following the COVID-19 pandemic. To mitigate the effect of COVID-19 on businesses, the Chinese government, through the People’s Bank of China (PBC), financial institutions, and the various government agencies, reacted by supplying liquidity support to the private sector, mainly for small and medium-sized enterprises (SMEs). Some of the financial policies implemented were: (a) the granting of CNY 500 billion to SMEs and agricultural enterprises; (b) the granting of CNY 300 billion to enterprises directly engaged in the transportation, production, and sale of vital medical and life supplies; and (c) loan rescheduling (Zhang et al., 2020). Conversely, the COVID-19 pandemic exacerbated global uncertainties with uncertainties well-known to be detrimental to domestic credit (Gozgor et al., 2019). In light of these developments, the following questions remain: (1) has COVID-19 influenced domestic credit to the private sector? (2) did the size of the bank matter? (3) What is the impact of COVID-19 shocks (innovations to COVID-19) on the availability of domestic credit to the private sector? To address these questions, we dissect the banking sector data into aggregate, large banks[1], small banks[2], and the four largest national-operating state-owned commercial (Big Four)[3] banks to see if the COVID-19 pandemic explains changes to domestic credit to the private sector, taking into account inflation, the exchange rate, and money supply.

We contribute to the recent work on the impact of COVID-19 on the financial sector in the following ways. First, this study is the first to examine the impact of COVID-19 on domestic credit to the private sector. Extant studies on the impact of COVID-19 on the financial sector have concentrated on the stock market returns and volatilities (Gil-alana & Claudio-Quiroga, 2020; Kp, 2020; Narayan et al., 2020; Salisu & Sikiru, 2020; Sharma, 2020), exchange rate (Narayan, 2020a, 2020b) and insurance market development (Wang et al., 2020). This study complements the literature by examining the impact of the pandemic on domestic credit to the private sector by using the banking industry as a case study. It is well established in the literature that financial development measured by domestic credit to the private sector spurs economic growth (Appiah‐Otoo & Na, 2020; King & Levine, 1993). However, recent evidence shows that access to more finance is detrimental to growth (Law & Singh, 2014). Knowing the role of COVID-19 in credit growth will enable policymakers to address dangers associated with rapid credit growth. Moreover, we examine the impact of COVID-19 on domestic credit by considering the size of banks. The link between bank size and lending remains debatable. In the case of China, there is credit rationing and channeling of credit to state-owned enterprises that are the fundamental recipients of loaning by large banks (Allen et al., 2005). These disparities in credit allocation demand examining the impact of COVID-19 on domestic credit by considering the size of banks. Finally, we examine the impact of innovations to COVID-19 (COVID-19 shocks) on domestic credit in China. Although the COVID-19 pandemic started in Wuhan, China in late December 2019, China has been very proactive in abating the spread of the virus. The use of the impulse response analysis under the framework of the vector autoregressive model shows the short-and long-run variations of COVID-19 on domestic credit which enables good policies.

We test the hypothesis that COVID-19 confirmed cases and attributable deaths have a statistically significant and positive effect on domestic credit. Using the ordinary least squares estimator, we discover that an increase in COVID-19 confirmed cases and attributable deaths significantly increase domestic credit in China which confirms our hypothesis. The impulse response analysis shows that the response of domestic credit to COVID-19 confirmed cases and attributable deaths was positive in both the short- and long-run.

The rest of the study is as follows. The next section offers the methodology which composes of the data and the model. Section III contains the results and discussions accompanied by the conclusion and policy implications in Section IV.

II. Data and Methodology

A. Data

We use daily data for the period January 01, 2020 to June 30, 2020. This data sample is dictated by the availability of Chinese data. The sample covers six variables: domestic credit to the private sector; confirmed cases of COVID-19; deaths from COVID-19; inflation; exchange rate; and money supply. The source of COVID-19 data is the World Health Organization Coronavirus Disease (COVID-19) Dashboard[4]. The source of domestic credit to the private sector, money supply, and exchange rate data are from the PBC[5]. Finally, the source of inflation data is the National Bureau of Statistics[6]. The data on domestic credit to the private sector was further disaggregated into large banks, small banks, and the Big Four banks. Table 1 present the descriptive statistics of the variables over the study period.

B. Methodology

We estimate the following model:

where represents domestic credit to the private sector (further categorized into domestic credit to the private sector by large banks, small banks, and the Big Four banks) at time t. denotes COVID-19 confirmed cases; denotes inflation; represents exchange rate; represents money supply; and represents the error term. We estimate Equation (1) with the ordinary least squares estimator.

We expect to have a statistically significant and positive relationship with domestic credit to the private sector. We expect and to have a statistically significant and negative relationship with domestic credit to the private sector. Finally, we expect to have a statistically significant and positive relationship with domestic credit to the private sector.

III. Empirical Findings

A. Regression results

Table 2 (Panel A) presents the results for the impact of confirmed cases on domestic credit. Model 1 presents the results for the full sample, whilst Models 2-4 present the results for large banks, small banks, and the Big Four banks. The results show that confirmed cases have a significant and positive effect on domestic credit. This implies that the COVID-19 pandemic promotes domestic credit to the private sector; however, the magnitude of the impact is very small. This supports our hypothesis that COVID-19 has a statistically significant and positive effect on domestic credit. These findings also indicate that the size of banks does not matter in terms of credit allocation to the private sector.

Inflation significantly decreases domestic credit in all sample of data. An increase in inflation decreases domestic credit by 0.03% (full sample), 0.03% (large banks), 0.04% (small banks), and 0.02% (Big Four banks). The significant negative effect of inflation on domestic credit is in line with the findings of Gozgor et al. (2019), who study 139 countries and find that inflation reduces domestic credit to the private sector.

Exchange rate significantly decreases domestic credit in all samples of data. The results show that an increase in exchange rate decreases domestic credit by 0.39% (full sample), 0.33% (large banks), 0.45% (small banks), and 0.26% (Big Four banks).

Money supply significantly increases domestic credit. An increase in money supply increases domestic credit by 0.78% (full sample), 0.72% (large banks), 0.87% (small banks), and 0.79% (Big Four banks).

In Table 2 (Panel B), we use COVID-19 attributable deaths to re-estimate the model. The results are not significantly different from those obtained in Table 2 (Panel A).

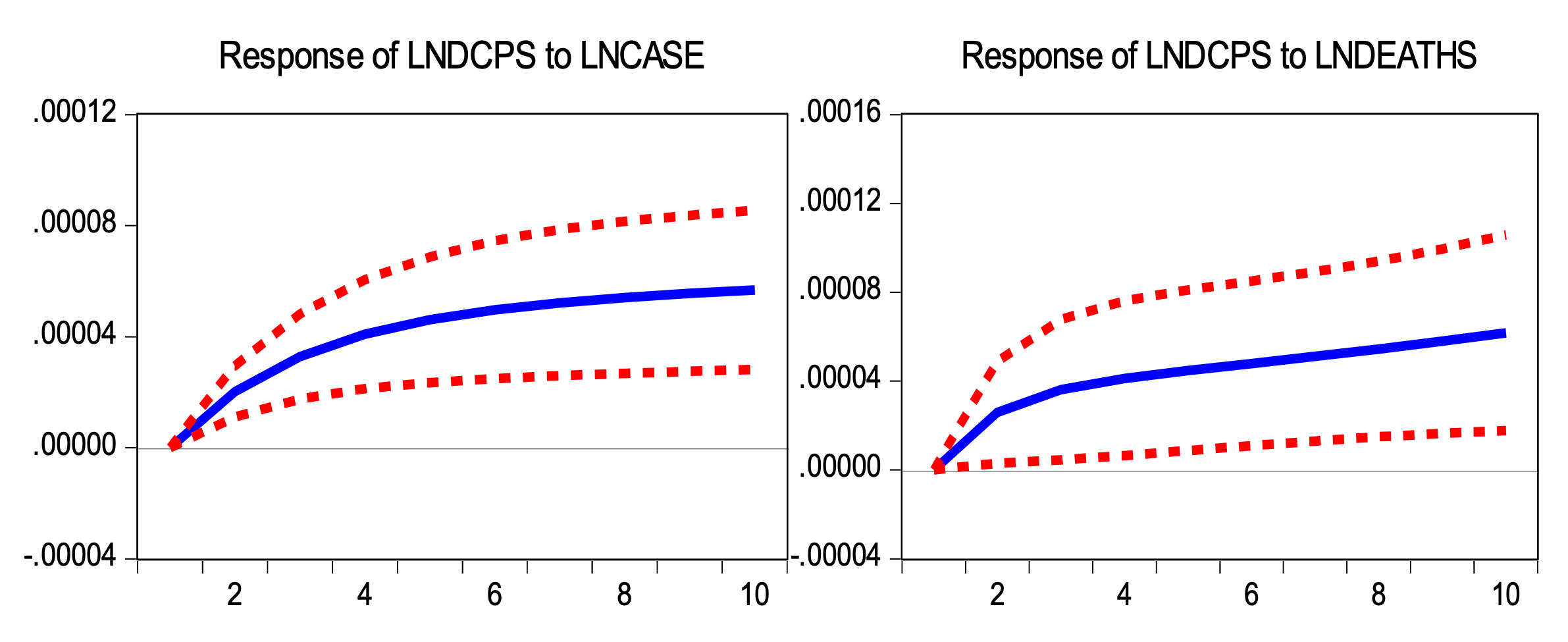

B. Impulse response analysis

In this section of the study, we examine shocks (innovations) from confirmed cases and deaths on domestic credit to the private sector. The results are presented in Figure 1. The results show that the response of domestic credit to confirmed cases and deaths shocks’ is positive in both the short- and long-run.

IV. Conclusion

In this paper, we examined whether: (a) COVID-19 influences domestic credit to the private sector (2); (b) the size of the bank matters; and (c) COVID-19 shocks impacted domestic credit to the private sector. We find that an increase in COVID-19 confirmed cases and attributable deaths significantly increase domestic credit in China; however, the magnitude of the impact is very small. The impulse response analysis reveals that the response of domestic credit to COVID-19 shocks was positive in both the short- and long-runs.

In view of these findings, we recommend the PBC to reduce the cash reserve requirements in the banking sector to stimulate credit to the private sector as suggested by Nguyen & Boateng (2013).

Large-sized state-owned commercial banks are those with total assets greater than or equal to 2 trillion Yuan.

Medium & small-sized state-owned commercial banks are those with total assets less than 2 trillion Yuan.

The Big Four banks are the Bank of China, the China Construction Bank, the Agricultural Bank of China, and the Industrial and Commercial Bank of China.