I. Introduction

This note tests whether a dynamic Student’s t copula with Markov-switching autoregressive conditional heteroskedasticity (MSGARCH) recognizes regime changes in the dependence between Asia-Pacific Islamic stocks and gold and outperforms non-MSGARCH models in estimating value at risk (VaR). The responsiveness of Asia-Pacific Islamic stocks to the pandemic has been well documented (Salisu & Sikiru, 2020). However, no conclusive impact of gold in reducing the risk of stock markets during the COVID-19 outbreak is observed. For instance, gold is not a safe haven asset for Chinese equity markets (Corbet et al., 2020). Salisu et al. (2021) find the gold market is able to function as a safe haven. In this spirit, this note captures regime changes to revisit the hedge effectiveness of gold against the risk of Islamic and conventional stock markets.

This paper hypothesizes a negative conditional dependence between Asia-Pacific Islamic stocks and gold in a high-volatility regime. This hypothesis is motivated by the ability of gold to minimize the risk of stocks during the pandemic, which has been well documented (Padhan & Prabheesh, 2021). One limitation of the literature is that mostly non-MSGARCH models are used to measure the hedge effectiveness of gold against the risk of stocks during the pandemic (Ajmi et al., 2021; Corbet et al., 2020; Fakhfekh et al., 2021; Jeribi & Ghorbel, 2021; Sikiru & Salisu, 2021).

This note uses daily time-series data and a regime-switching Student’s t copula. It concludes that an MSGARCH model with a Student’s t copula has the best fit. In addition, the dependence between gold and Islamic stocks exhibits tail symmetry. A robustness check (using conventional stocks and gold) shows similar results. The dependence between Islamic stocks and gold on the structural break is lower than for the dependence between conventional stocks and gold, suggesting stronger diversification benefits.

The remainder of the paper is organized as follows. Section II reveals the methodology. Section III presents the main findings. Section IV draws the conclusion.

II. Methodology

This note uses the Dow Jones Islamic Market Asian/Pacific Developed TopCap Index (Asian DJIM) to proxy for Islamic stocks (large- and mid-cap stocks located in developed Asia-Pacific markets. It also utilizes the Dow Jones Composite Average (DJCA), which represents large, well-known U.S. companies for comparison, and exchange-traded funds for gold (GLD). The indexes are retrieved from S&P Global (https://www.spglobal.com/spdji/en/). The whole sample covers from December 7, 2015,[1] to June 30, 2021, and two subsamples respectively cover the pre-COVID-19 pandemic period, from December 7, 2015, to March 10, 2020, and the COVID-19 pandemic period, from March 11, 2020,[2] to June 30, 2021.

This note begins with determining the margin of logarithmic returns by fitting the Glosten–Jaganathan–Runkle (1993) GARCH model, obtaining the standardized residuals, and applying a cumulative distribution function. This research follows Maneejuk & Yamaka (2019) to estimate a dynamic Student’s t copula, as follows:[3]

ρT,t= Δ WT0+ WT1ρT,t−1+ WT211010∑j=1F−11(ut−j)F−11(vt−j)

The analysis uses a dynamic Student’s t copula model with regime-switching estimation according to Fei et al. (2017) and Maneejuk & Yamaka (2019), as follows:[4]

ρT,tSt= Δ WT0St+ WT1StρT,t−1+ WT2St11010∑j=1F−11(ut−j)F−11(vt−j)

A two-regime model is estimated, ∈ {1,2}, where = 1 denotes a low-volatility regime and = 2 represents a high-volatility regime. This estimation is used because the volatility predictions of standard GARCH-type models are potentially less capable of extracting the actual volatility in the case of regime changes. This study also evaluates one-day-ahead VaR forecasts (Ardia et al., 2019). A total of 50% of the data are out of sample and estimated by maximum likelihood every 50 observations. The dynamic quintile (DQ) and the conditional coverage (CC) tests determine if the forecasts fit (Christoffersen, 1998; Engle & Manganelli, 2004).

III. Main Findings

Table 1 shows the models exhibit no heteroscedasticity or serial correlation in the estimated standardized residuals, based on Ljung–Box Q-statistics and autoregressive conditional heteroskedasticity statistics, suggesting strong goodness of fit.[5] Moreover, the reaction coefficients are less than 0.1, indicating that volatility is not very sensitive to market events. The γ value is positive and significant for Islamic and conventional stocks, suggesting a leverage effect. This result indicates that negative sentiment has a more significant effect than positive news on conditional variances. All the estimates of α + β are above 0.9, implying that shocks in the stock and gold markets have highly persistent volatility.

Table 2 shows the Student’s t copula with MSGARCH estimation is the best-fitting model due to the lower Akaike information criterion. Therefore, this discussion focuses on models with regimes K= 1 and K = 2. For instance, the parameters are mostly significant and negative, implying low persistence.

Focusing on the whole sample period, the parameter is only significant for the two-regime estimation (K = 2) for Islamic stocks and gold, indicating substantial variation. However, the variation parameter is quite a bit larger than the parameter in regime K= 1, showing the predominance of dynamic effects.

No predominance of dynamic effects is found for the COVID-19 period. In addition, the variation parameter is smaller than the persistence parameter and more significant, implying volatility persists for longer following a turbulent market.

Further, the probability of remaining in the high-volatility regime (P22) is higher for the relation between conventional stocks and gold than for that between Islamic stocks and gold, implying weaker diversification benefits. In addition, P11 is highly persistent (above 0.8) during the pandemic.

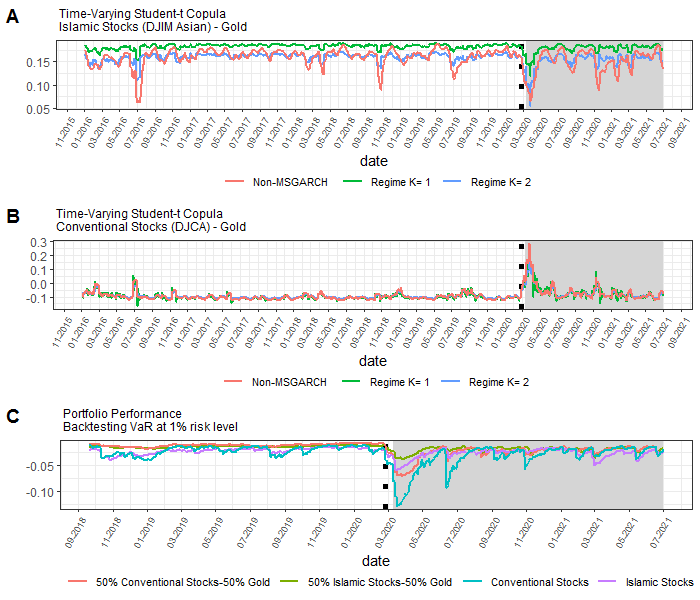

Figure 1 reveals the time path of the best fitted copula. The conditional dependence between Islamic stocks and gold in the one-regime model is higher than the dependence in the two-regime model while the increased dependence of the relation between conventional stocks and gold on the structural break implies lower diversification benefits.

In Figure 1A, focus on the dotted vertical lines shows the dependence between gold and Islamic stocks to be decreasing. However, Figure 1B indicates that the dependence between gold and conventional stocks is increasing. This result implies that, in periods of turmoil, gold tends to be a good hedge against the risk of Islamic stocks. This finding is supported by Figure 1C. Finally, the copula with a single-regime specification outperforms the other models when forecasting the VaR, as shown in Table 3.

IV. Conclusion

This paper finds the dependence of Student’s t copula between stocks and gold to be negative and significant, which indicates tail symmetry. This result reveals the dependence does not emerge during turbulent market events. In addition, the dependence between Islamic stocks and gold is weaker than that between conventional stocks and gold at the structural break, implying greater hedge effectiveness.

Further, the present work shows that the equally weighted portfolio of stocks and gold has lower risk compared to an unhedged strategy during the COVID-19 outbreak. Specifically, gold is more powerful at reducing the risk of Islamic stocks than that of conventional stocks. Moreover, this note finds a time-varying Student’s t-copula with regime-switching GARCH to be the best-fitting model. This result suggests the predictability of the degree of dependence between stock markets and other commodities can be evaluated by using the fear index as a predictor.

December 7, 2015, was the launch date of the DJIM Asian.

The World Health Organization announced COVID-19 to be a global pandemic on March 11, 2020.

This paper uses the R package DynamicCOP (available at https://rdrr.io/github/woraphonyamaka/DynamicCop/) and finds that a Gaussian copula does not fit.

This note uses the R package MSGARCH (available at https://CRAN.R-project.org/package=MSGARCH; see (Ardia et al., 2019)).

The diagnostic tests for the pre-COVID-19 and COVID-19 periods show similar results. Due to limited space, they are not tabulated here.