I. Introduction

The sharp increase in uncertainty of the current coronavirus disease (COVID-19) pandemic has a huge effect on the real economy and the financial sphere. Recently, several papers examined the effect of COVID-19 on the stock market risk by either focusing on one specific market or international markets. These papers use market return volatility to measure market risk. Albulescu (2020) and Baker et al. (2020) show that the COVID-19 pandemic has a significant positive impact on the US stock market volatility. Zhang et al. (2020) and Zaremba et al. (2020) find that the outbreak of COVID-19 substantially increases the international stock market risk. Mishra et al. (2020), Narayan et al. (2021), and Oliyide et al. (2022) confirm a significant impact of COVID-19 on the stock returns in India and G7 stock markets.

Different from the previous papers to explore the static impact of COVID-19 pandemic on the stock market (see Zaremba et al., 2020; Zhang et al., 2020), our paper applies the panel VAR model and impulse-response functions and concentrates on examining the dynamic effect of world pandemic uncertainty (using the uncertainty index of Ahir et al. (2022)) on the international stock market crash risk from 1996 to the end of 2021. Our paper distinguishes the different impacts of world pandemic uncertainty on the advanced and emerging stock markets. We find that the world pandemic uncertainty has a positive and significant effect on the international stock market crash risk. The impact of world pandemic uncertainty on the crash risk is largest in the first quarter (around 18%) and significantly fades away in the next three quarters after the shock. A one-standard deviation increase in the pandemic uncertainty shock (i.e., COVID-19 uncertainty shock) increases the stock market crash risk to by around 70%. Moreover, our findings are robust for developed and emerging markets, and for alternative measures of crash risk and world pandemic uncertainty.

The remainder of this paper is organized as follows. Section II describes the methodology and data. Section III discusses the empirical results and Section IV concludes.

II. Methodology and Data

A. Panel VAR model

Panel VAR builds upon and extends the traditional VAR approach to a panel setting that allows for individual unobserved heterogeneity (Holtz-Eakin et al., 1988). The approach of this section is similar to that of Love and Zicchino (2006). In this paper, we build the panel VAR model and impulse-response functions to examine the dynamic effect of world pandemic uncertainty (WPU) on the country-specific stock market crash risk. Mathematically, a p-order VAR model is specified as follows:

Yi,t=α+p∑j=1βjYi,t−j+fi+εt

In the panel VAR model, Y includes stock market crash risk (NCSKEW), world pandemic uncertainty (WPU), stock market returns (RET), GDP growth (GROWTH), price level change (CPI), and foreign exchange rate change (FX). These variables are used for each stock market. Economic growth is regarded as a target variable, while price level change is regarded as a monetary policy shock. The panel VAR procedure requires that the underlying structure is heterogeneous across each cross-sectional unit, which can be achieved by allowing for fixed effects fi. We use forward mean-differencing, also known as the Helmert procedure, to remove the mean of all future observations available for each market and time in order to preserve the orthogonality between transformed variables and lagged independent variables (Love & Zicchino, 2006). After eliminating fixed effects by differencing, we apply the panel GMM estimation, where lagged regressors were used as instruments in order to estimate coefficients more consistently.

In line with Jurado et al. (2015) and Bakas and Triantafyllou (2020), we use a recursive identification procedure, whereby the world pandemic uncertainty measures are placed last in the panel VAR ordering since in this order the effects of pandemic uncertainty shocks on the other variables in the system are measured after removing all the variation in pandemic uncertainty attributable to shocks to the other endogenous variables in the system. When the effect of pandemic uncertainty shocks is significant, then pandemic uncertainty really has an important impact on the stock market crash risk. Hence, the panel VAR ordering is [NCSKEW, RET, GROWTH, CPI, FX, WPU].[1]

For the measurement of country-specific crash risk, we calculate crash risk (NCSKEW) in line with Callen and Fang (2015). We first estimate country-specific daily residual returns from the following MSCI All Country World Index (ACWI) regression for each country and each quarter in Eq. (2) (Hutton et al., 2009).

ri,t=αi+β1,t−1rm,t−1+β2,trm,t+β3,tri,t+1+εj,t

where ri,t is the stock returns of country i on day t and rm,t is the daily returns of the MSCI All Country World Index.

We define country-specific daily returns, Ri,t as the natural logarithm of one plus the residual returns from Eq. (2). Our main country-specific measure of the stock price crash risk is the negative coefficient of skewness of country-specific daily returns (NCSKEW) computed as the negative of the third moment of each country-specific daily returns, divided by the cubic standard deviation as below:

NCSKEWi,T=−(n(n−1)2/3∑R3i,t)(n−1)(n−2)(∑R2i,t)2/3

where n is the number of observations of country-specific daily returns during quarter T. An increase in NCSKEW shows greater left skewness in the distribution of country-specific returns and suggests higher market crash risk.

B. Data

In this paper, we collect MSCI ACWI stock market indexes across 23 developed and 27 emerging markets from Datastream.[2] We calculate the quarterly stock market crash risk (NCSKEW) and the quarterly log returns measure (RET) for each stock market index. The world pandemic uncertainty index (WPUI) is based on the work of Ahir et al. (2022) and measures economic uncertainty related to pandemics and other disease outbreaks across the world as reflected in the Economist Intelligence Unit country reports. We collect the world pandemic uncertainty index from https://worlduncertaintyindex.com/. We use the log difference of GDP, CPI, and foreign exchange rate to measure GDP growth, price level change, and foreign exchange rate change. These variables are collected from the Global Economic Monitor database and Datastream. The quarterly dataset used in this paper covers the period from January 1996 to December 2021 (1996Q1–2021Q3).

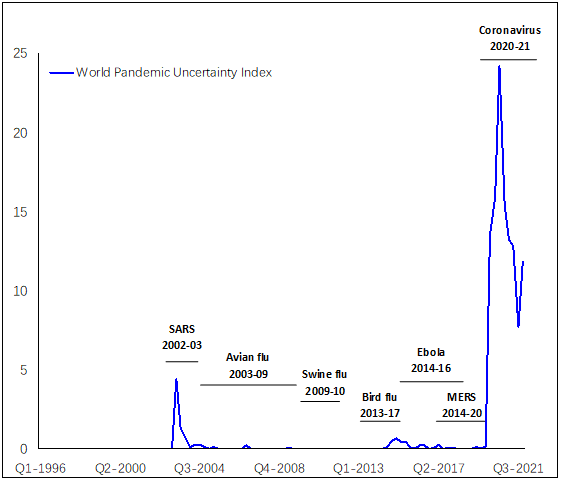

Figure 1 shows main SARS, Avian flu, Swine flu, Bird flu, Ebola, MERS, and Coronavirus (COVID-19). We observe COVID-19 pandemic uncertainty is much higher than the rest of the pandemic uncertainties.

III. Empirical Analysis

A. Main results

In this subsection, we apply the panel VAR and impulse-response functions (IRFs) to analyze the response of the stock market crash risk to a one-standard deviation increase in the world pandemic uncertainty shock. In the panel VAR model, we control for stock market returns, economic growth, inflation, and foreign exchange rate change, which take into account the possible dynamic interactions of the pandemic uncertainty with stock performance and macroeconomic factors.[3] In Figure 2, it is evident that a positive shock to pandemic uncertainty increases crash risk by around 18% in the first quarter after the hock and the effect remains significantly positive for about three quarters, since the 95% confidence interval includes zeros after three quarters.[4]

B. World pandemics uncertainty of COVID-19

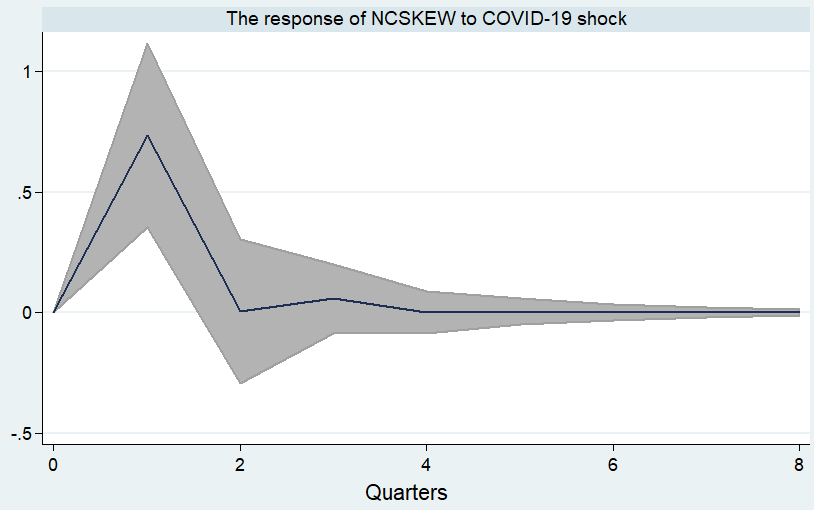

In light of previous papers that investigate the effect of COVID-19 pandemic on the stock market risk, we also examine the world COVID-19 pandemic uncertainty shock on the market crash risk from 2020Q1 to 2021Q3.[5] Figure 3 confirms the positive response of the stock market crash risk to the pandemic uncertainty shock. It is evident that a positive shock to the pandemic uncertainty increases crash risk by around 70% in the first quarter after the shock, which is three times as large as the result in Figure 2, indicating a larger shock of COVID-19 to the global stock market crash risk. The positive effect fades away very quickly in about two quarters after the initial shock.

C. Developed markets vs emerging markets

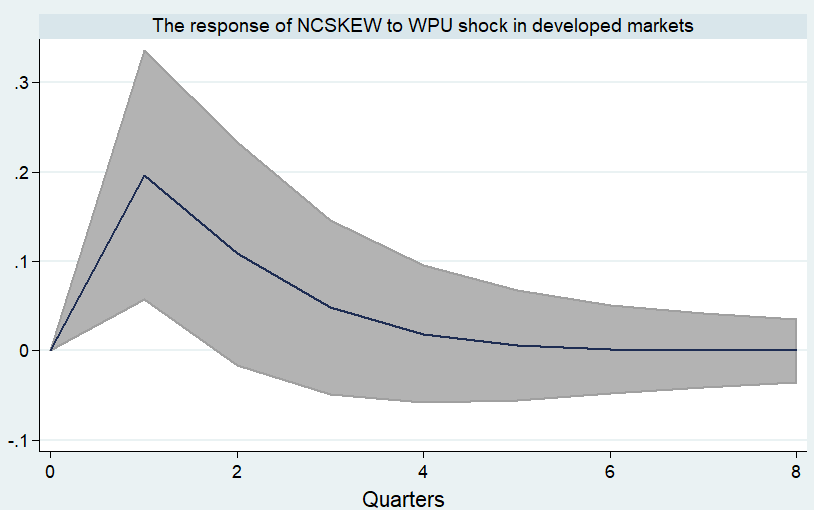

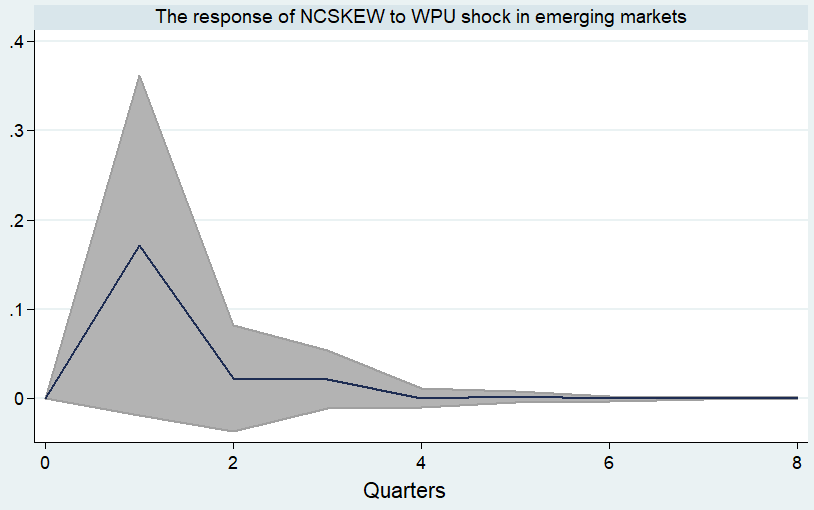

To detect the differential effects between developed and emerging markets, we apply the panel VAR model and impulse-response functions to investigate the response of stock market crash risk to a one-standard deviation increase in the pandemic uncertainty shock. In Panels A and B of Figure 4, we observe that a positive pandemic uncertainty shock increases around 20% of the stock market crash risk in one quarter after the shock, while the effect remains significant for two quarters in developed stock markets. In emerging stock markets, we find that a positive pandemic uncertainty shock increases about 17% of the stock market crash risk in one quarter after the shock and it quickly fades afterwards.

_world_pandemic_uncertainty_shock_and_stock_market_crash_risk_in_developed_market.png)

_world_pandemic_uncertainty_shock_and_stock_market_crash_risk_in_emerging_markets.png)

D. Robustness checks

In this subsection, we conduct several robustness checks on our results. These checks relate to the measures of stock market crash risk and world pandemic uncertainty.

Firstly, we use an alternative crash risk measure (DUVOL) of Callen and Fang (2015). The results show that a positive shock to pandemic uncertainty increases the crash risk by around 8% in the first quarter after the one-standard deviation shock. In the second quarter, the effect drops to 3% and then diminishes.[6]

Secondly, we use an alternative stock market crash risk measure. We add daily smoothed new cases of COVID-19 per million from Ritchie et al. (2020) in Eq. (2), obtain the regression residuals, and then calculate the stock market crash risk by Eq. (3). The logic is that a shock like COVID-19 can impact this regression residuals and the calculated crash risk (see Davis & Ng, 2022).[7] We obtain very similar findings; that is, a positive shock to pandemic uncertainty increases the crash risk, which reaches its peak in the first quarter after the initial shock and the effect remains significantly positive for about three quarters.

Thirdly, we use the index of discussion about pandemics in Ahir et al. (2022) as an alternative measure of world pandemic uncertainty. We still find a positive response of stock market crash risk to the pandemic uncertainty shock. The effect reaches 5% in the first quarter and slowly dies down in the third quarter.

Lastly, we add the country-level world uncertainty index (Ahir et al., 2022) to our panel VAR model. We still find a positive response of stock market crash risk to pandemic uncertainty shock. The effect reaches 15% in the first quarter and slowly dies down in the third quarter after the shock.

IV. Conclusion

This paper aims to examine the dynamic impact of world pandemic uncertainty on the crash risk of 50 international stock markets. The results show that world pandemic uncertainty has a positive impact on the crash risk. The effect is largest in the first quarter and significantly diminishes in three quarters after the shock. The positive impact of COVID-19 on the stock market crash risk is huge. Our results related to the dynamic impact of world pandemic uncertainty are robust for developed and emerging markets, as well as, for alternative measures of crash risk and world pandemic uncertainty.

Funding

We gratefully acknowledge the financial support from the National Natural Science Foundation of China (Grant No. 71971133), the National Social Science Foundation of China (Grant No. 21BGL270), Humanities and Social Sciences Research Youth Fund from Ministry of Education of China (Grant No. 20YJC790194) and the Shanghai Sailing Program (Grant No. 20YF1413100).

For the panel VAR model specification, we select one lag of regressors as an optimal lag length in our panel VAR model in line with moment and model selection criteria (MMSC) (Andrews & Lu, 2001). The results from this test can be obtained from the authors upon request.

We try the different orders of WPU in our panel VAR model from the first to the last. We find that the effect of different orders of WPU in the panel VAR on the our findings is very small.

The detailed information related with the MSCI ACWI stock market indexes and the 50 international stock market indexes are reported on the webpage: https://www.msci.com/our-solutions/indexes/acwi.

The developed stock markets include Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Poland, South Africa, Spain, Sweden, United Kingdom, and United States.

The emerging stock markets include Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, South Korea, Kuwait, Malaysia, Mexico, Pakistan, Peru, Philippines, Portugal, Qatar, Russia, Saudi Arabia, Singapore, Switzerland, Taiwan, Thailand, Turkey, and United Arab Emirates

We estimate the orthogonalized IRFs using a Cholesky decomposition based on our panel VAR ordering.

We check the stability condition of the panel VAR and find that all the eigenvalues lie inside the unit circle, which show panel VAR satisfies the stability condition. Besides, we use pairwise panel Granger causality tests for world pandemic uncertainty and stock market crash risk and find that world pandemic uncertainty Granger causes the stock market crash risk, but stock market crash risk does not Granger cause the world pandemic uncertainty, which meets our expectation. The results from this analysis can be obtained from the authors upon request.

Alternatively, we apply the simple impulse-response functions to explore the response of the stock market crash risk to a one-standard deviation increase in the world pandemic uncertainty shock. The results are consistent with our main finding. The results from this analysis can be obtained from the authors upon request.

Because of the limited time-series observations from 2020Q1 to 2021Q3, we use the bivariate panel VAR with stock market crash risk and world COVID-19 pandemic uncertainty measures here. In this exercise, we have a total of 350 observations in the panel VAR model.

We calculate tail risk of stock market returns to measure the country-specific stock market crisis. By running the panel VAR model, we find that WPU has a significant and positive effect on the country-specific stock market crisis.

Robustly, we add smoothed new deaths of COVID-19 per million in Eq. (2), obtain regression residuals, and then calculate stock market crash risk. Again, we obtain the similar findings as Figure 2. We collect daily smoothed new cases of COVID-19 per million and daily smoothed new deaths of COVID-19 per million from https://ourworldindata.org/coronavirus.