I. Introduction

Since cryptocurrencies first appeared in 2009, investors, professionals, and academics have questioned their potential to hedge conventional assets. Furthermore, various crises have occurred in the previous decade, including the latest COVID-19 outbreak and the Russia-Ukraine conflict. The epidemic and conflict have increased uncertainty and investment risk, in global financial markets. In these cases, investors strive to lower their investment risk and achieve optimum portfolio diversification by including new financial assets, such as Bitcoin. This is due to gold’s inability to maintain its historic function as a robust safe haven in the post-global financial crisis era (Chkili et al., 2021). Bekiros et al. (2017) and Shahzad et al. (2019) explain gold’s limited capacity to hedge by accelerating the financialisation of the commodities market and the response of gold prices to various events in recent years.

Despite the variety of cryptocurrencies, Bitcoin is perhaps the world’s most frequently used currency. Compared to other cryptocurrencies, Bitcoin has held the top position for the last ten years, accounting for 51% of total cryptocurrency asset capitalisation. Furthermore, the Bitcoin market has witnessed a rapid expansion over the previous decade. Bitcoin is the most significant cryptocurrency in terms of size and volume traded. By 2021, it has reached a market capitalisation of about $1 trillion.

The rise of Bitcoin as a new asset has caused concerns about its capacity to compete with gold in its traditional position as a safe haven. According to Baur and McDermott (2010) and Baur and Lucey (2010), gold may be used as a hedge against stock market volatility and as a safe haven during difficult market situations. Recent works, however, show varied outcomes based on the empirical techniques and sample countries under review. For example, Chkili (2016) and Mensi et al. (2018) argue that gold provides an inspirational role in conventional and Islamic market investments, making it less risky. However, Akkoc and Civcir (2019) demonstrate the existence of time-varying co-movement between gold and the Turkish stock market during periods of extreme volatility, indicating that gold cannot be regarded as a safe haven against volatility risk.

From a risk standpoint, an asset may be acceptable for investment if it is negatively correlated with another asset, because combining the two assets reduces risk dramatically. We follow Ratner and Chiu (2013) and distinguish between a diversifier, a hedge, and a safe haven. A diversifier is an asset that has a modest positive correlation with another asset. A weak (strong) hedge is an asset uncorrelated (negatively correlated) with another asset. A weak (strong) safe haven is an uncorrelated asset (negatively correlated) with another asset on average during periods of crisis. Because gold has long been seen as a hedge and a safe haven, these terms have already been ascribed primarily to gold (Baur & Lucey, 2010).

One of the fundamental investment practices is maintaining a diverse portfolio of asset classes, while decreasing risk exposure. As a result, investors are continuously looking for investment vehicles that do not correlate with their current holdings and provide more substantial hedging possibilities. Bitcoin can be considered as a new investment tool that can be utilised as a hedging and safe haven instrument.

The US economy is heavily dependent on energy consumption, and this need will only grow in the future. In 2022, oil was the most crucial energy source, accounting for 36% of total energy consumption. Consequently, we can reasonably assume that any change in oil prices will influence the US economy.

Dynamic copula theory is used in this work. The theory provides a versatile and strong tool for understanding and modelling multivariate distributions. The copula technique assumes that a joint distribution may be factored into the marginals and a dependency function termed a copula. The copula combines the marginal distributions to generate the joint distribution. The copula determines the dependency connection, while the marginals define the scale and form (mean, standard deviation, skewness, and kurtosis).

The main goal of this study is to look at the dynamic correlations between the US Islamic stock index returns (ISIR) and commodities like Bitcoin, gold, and crude oil. The findings will assist investors in selecting commodities appropriate for their portfolios, which will benefit the US economy in the long term. Our research provides empirical evidence on the volatility and correlations between Bitcoin, gold, crude oil, and the US Islamic stock index. It attempts to answer the following research question:

Which financial instruments should investors invest in for portfolio diversification during the bad and good times?

Using the most current data and appropriate methodology, the research attempts to provide the strategic inputs required by the investors looking to diversify their portfolios containing the US Islamic stock index, Bitcoin, gold, and crude oil.

Our paper is organised as follows. Section II describes the research methodology. Section III presents the data analysis and results in detail. Section IV summarises the study’s results employing excellent intuitions and relating them to earlier findings in the literature.

II. Research Methodology

A. Data

Our data set includes daily Bitcoin, crude oil, gold price returns, and Morgan Stanley Capital International (MSCI) US Islamic stock index returns from 01/08/2014 to 29/04/2022 (i.e., 2017 observations). The data are collected from Thomson Reuters Datastream.

B. Multivariate GARCH-DCC

This study adopts the Multivariate Generalised Autoregressive Conditional Heteroscedastic (MGARCH) model of Pesaran and Pesaran (2010) to answer its research question. We evaluated normal and t distributions to determine which model is at the optimal level. The results of the unconditional correlation coefficients should be sufficient to provide empirical support for our study question. As a complete approach to achieving the objective, we compute conditional cross-asset correlations via the MGARCH-DCC technique as below:

˜ρij,t−1(ϕ)=qij,t−1√qii,t−1qjj,t−1

where are given by

qij,t−1= ¯ρij(1− ϕ1− ϕ2)+ ϕ1qij,t−2+ ϕ2˜ri,t−1˜rj,t−1

In the above, is the (i,j)th unconditional correlation, and are estimated coefficients, where + < 1, and are the standardised returns.

The mean-reverting process is also tested by estimating Some diagnostic tests are performed for robustness checks. To further study the model, one can refer to Pesaran and Pesaran (2010).

III. Empirical Results and Discussions

We employed the MGARCH-DCC approach to estimate the diversification advantages of the chosen variables. Table 1 shows the maximum likelihood parameters and for the variables chosen, as well as the and that compare a multivariate normal distribution to a multivariate student t-distribution. Under the t-distribution specification, the maximum log-likelihood value is 22,204, which is substantially greater than that of the normal distribution, 21,833. The student t-distribution has a degree of freedom of 6.2 (less than 30), indicating that it is appropriate for capturing the fat-tailed feature of stock returns.

Table 2 shows the estimated unconditional volatilities on the diagonal, while the unconditional correlations are shown off the diagonal. The numbers in parentheses denote the unconditional volatility ranking from most significant to least. The findings show that Bitcoin and crude oil prices are more susceptible to speculative trade fluctuations. The US Islamic stock index is the second-lowest volatile variable, supporting the belief that the US economy is robust and healthy.

Finding the unconditional correlations between the chosen variables is more important to our study’s goals. Table 3 ranks the unconditional correlations (from highest to lowest) for all variables used for this investigation. The ranking shows two critical facts. First, gold and Bitcoin have the lowest correlation of all the variables under consideration (see notation ‘a’ in Table 3). Investors should incorporate gold and Bitcoin in their portfolios for maximum portfolio diversification advantages. However, Bitcoin’s extreme volatility (as seen in Table 2) limits its full potential as a hedging and diversification tool. Second, Table 3 shows that investors of the US Islamic stock index are better off diversifying in gold than Bitcoin or crude oil. Gold is an almost optimal hedge against inflation (Worthington & Pahlavani, 2007), and it has long been utilised as a safe haven amid financial, political, and economic crises. Dyhrberg (2016) notes that Bitcoin and gold are highly comparable. Both instruments respond similarly to other variables in his analysis, have similar hedging capabilities, and react symmetrically to good and negative news.

So far, our volatility and correlation assessments and conclusions have been performed on an unconditional basis. An unconditional basis indicates that we use the sample period’s average volatility and correlation. However, the assumption that volatility and correlation stay constant over a nearly eight-year period does not appeal to intuition. Volatility and correlation are more likely to be dynamic in character, and it is this element that the Dynamic Conditional Correlations (DCC) model used in this article emphasizes.

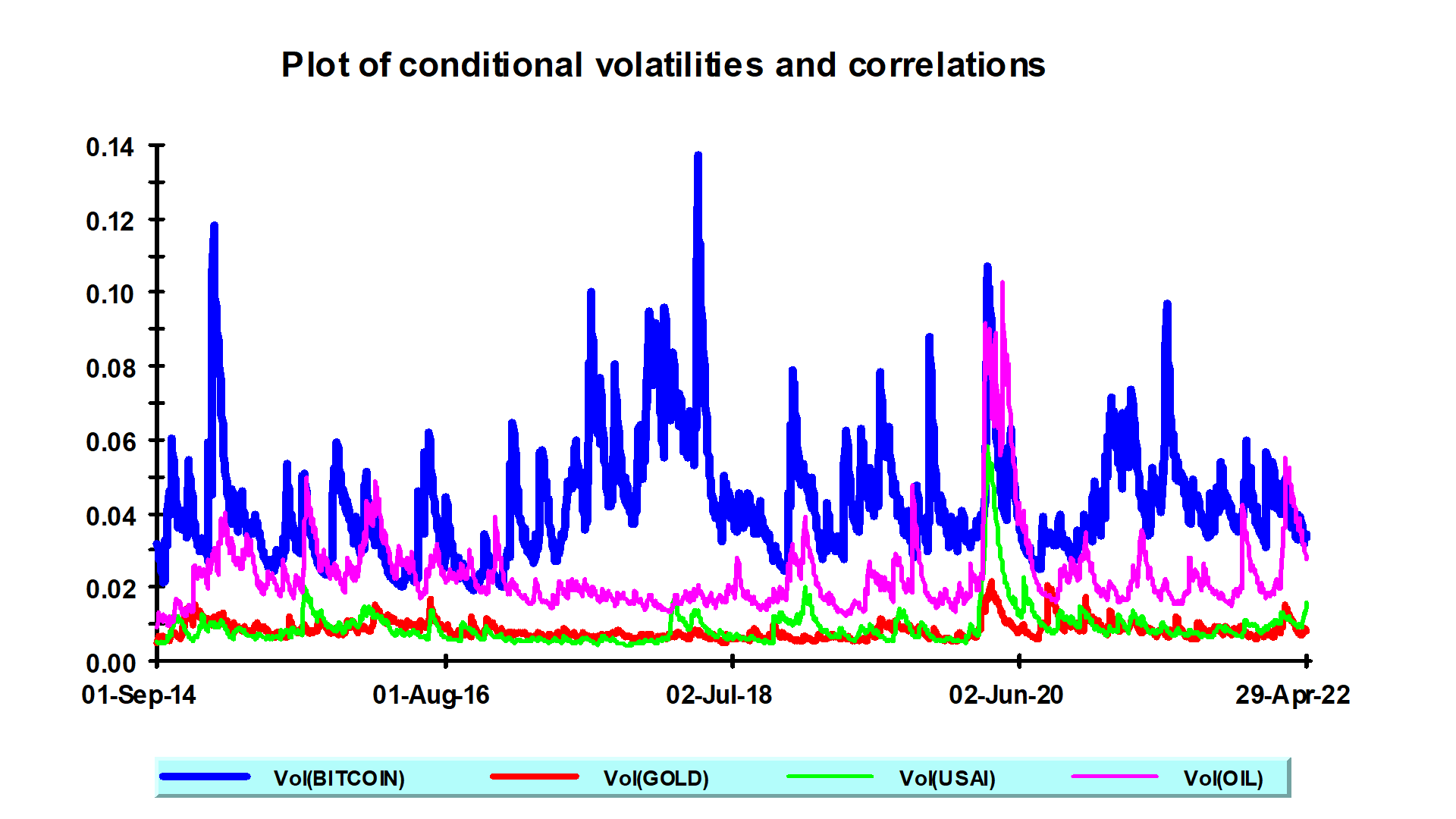

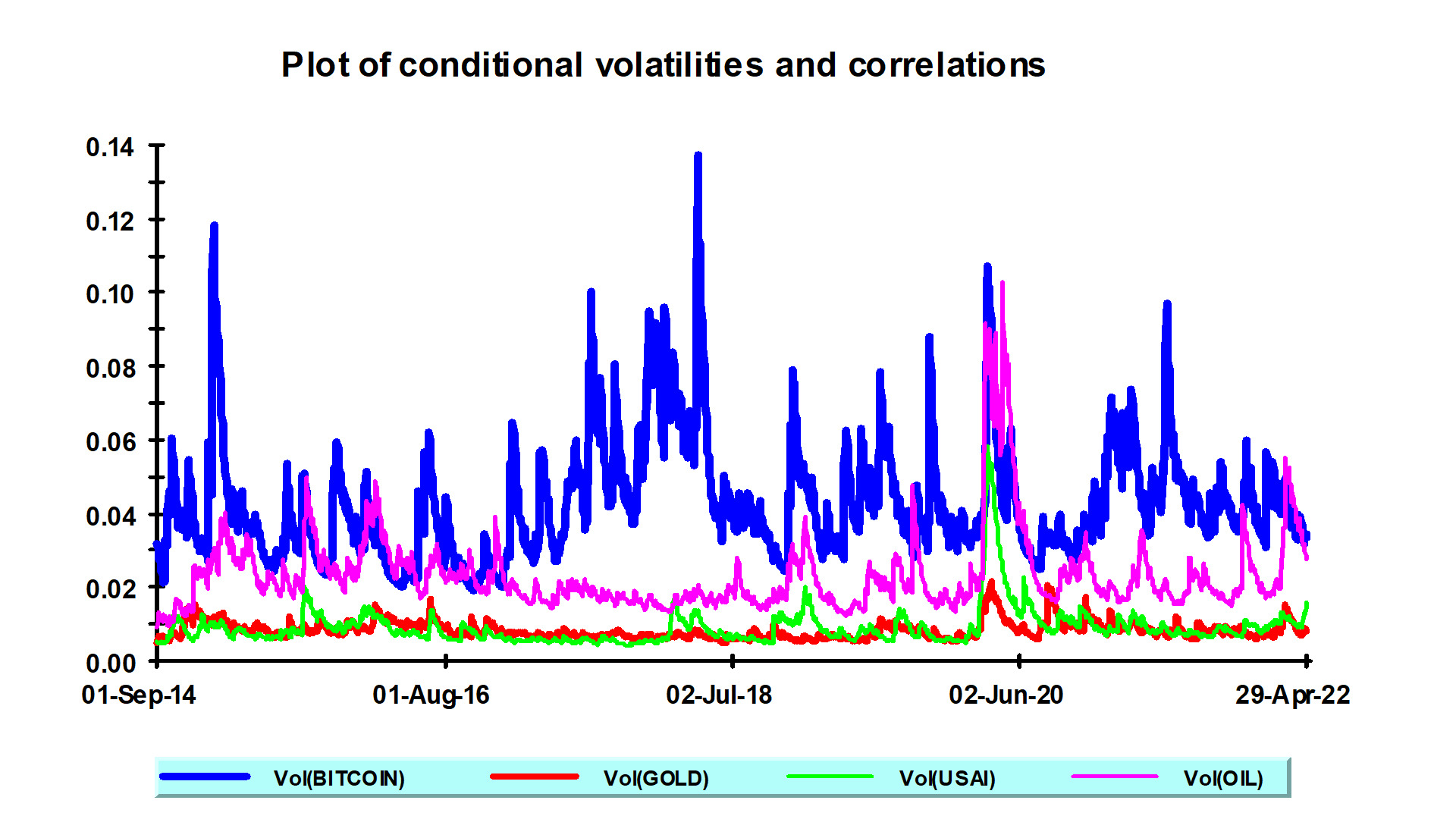

We begin by looking at the temporal dimension of volatility. During nearly eight years of research, we discovered that Bitcoin prices have the highest volatility compared to others. Gold has the lowest volatility over the period. Most of the variables increased significantly, in terms of volatility, with the start of the COVID-19 pandemic in 2020, suggesting a turbulent era. When the conflict between Russia and Ukraine began in 2022, the variables were not as volatile as they were during the epidemic era. As a result, investors did bear less risk during the conflict than during the epidemic. Based on Figure 1, we can infer that investing in Bitcoin is risky since it is highly volatile and unpredictable compared to other variables. As seen in Figure 1, gold is the least volatile commodity compared to the other variables, suggesting a solid investment too.

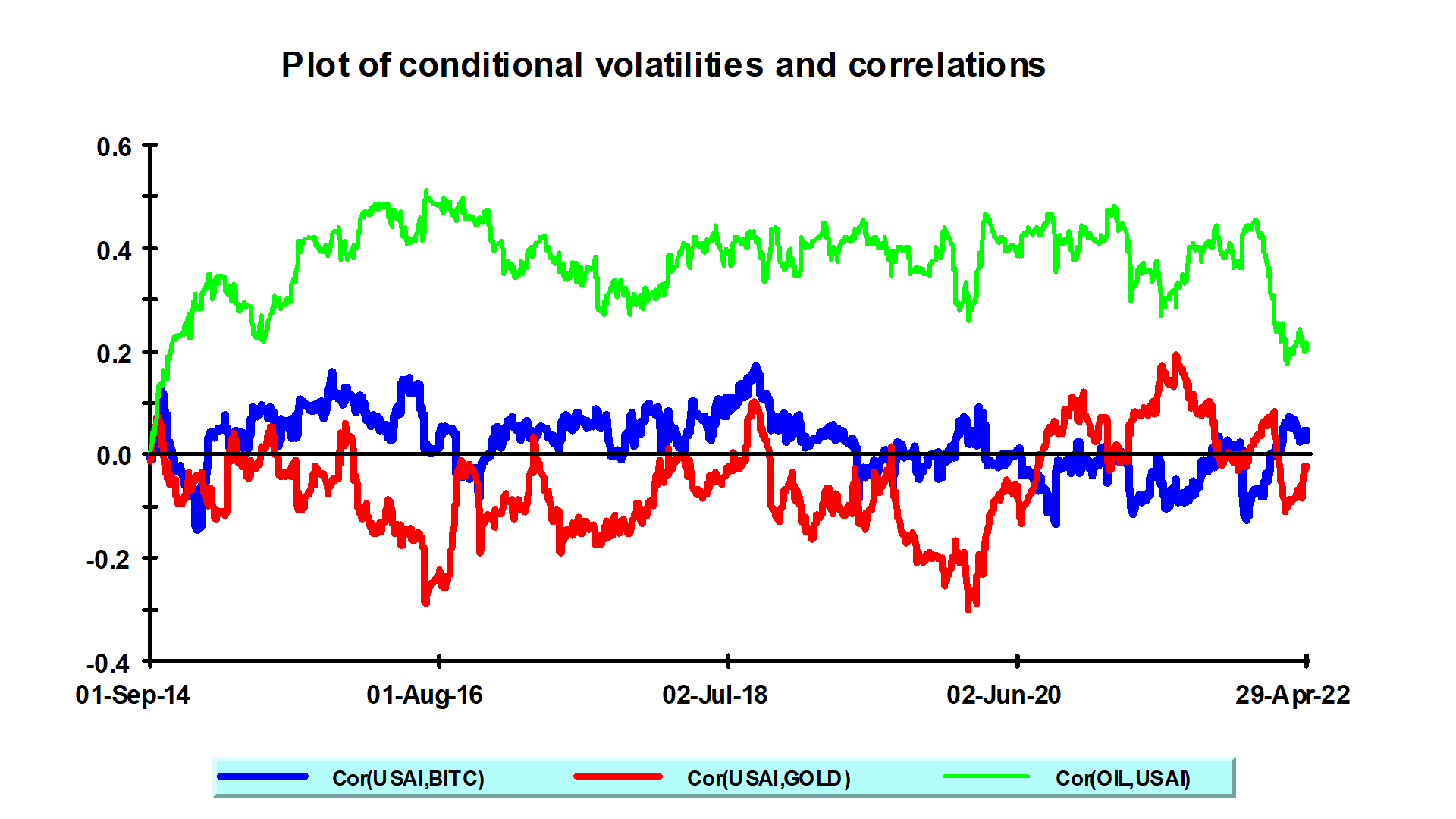

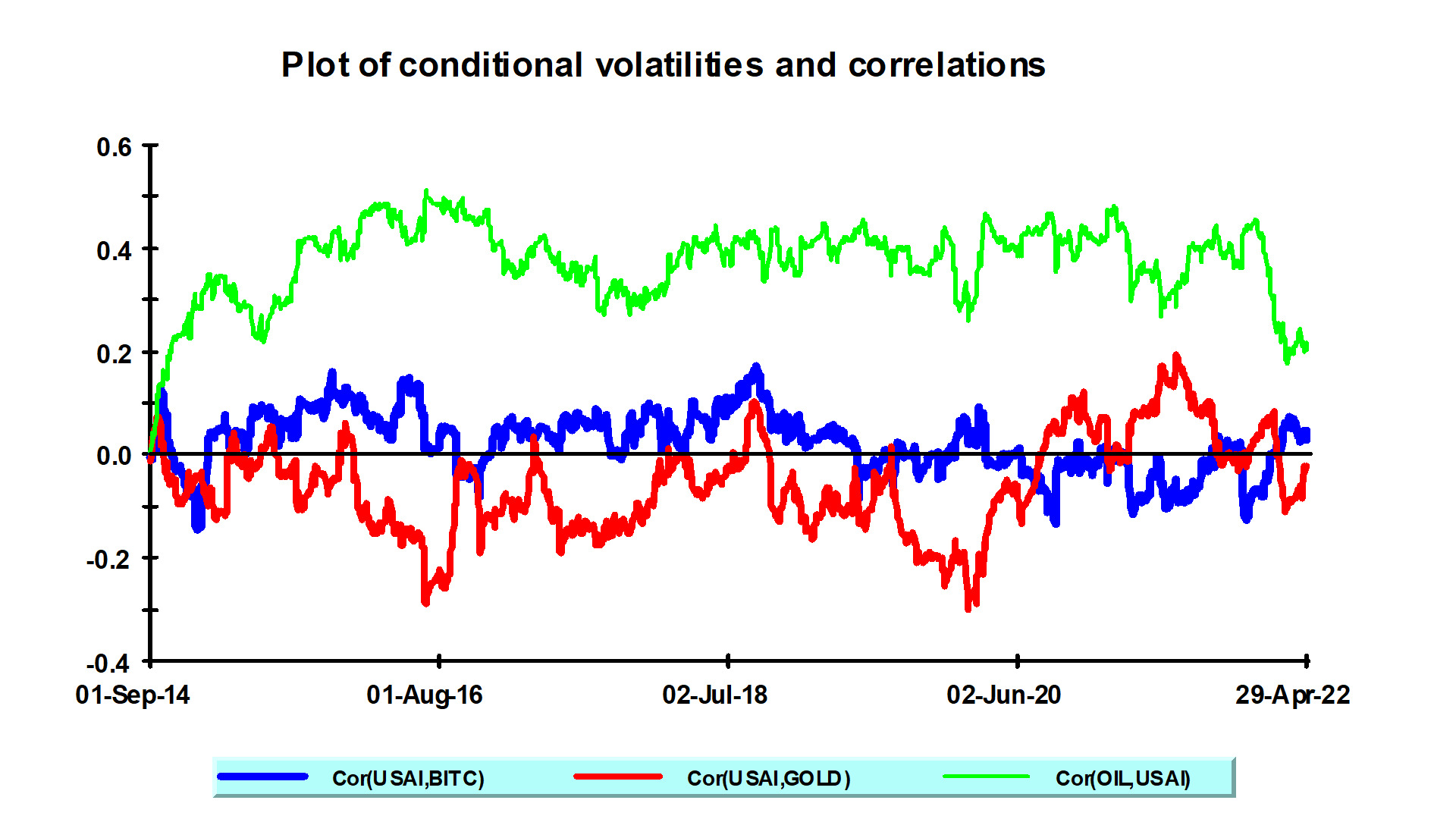

We examine the correlation between the US Islamic stock index and other commodities using conditional correlations, as shown in Figure 2. From 2014 until 2022, correlations of the US Islamic stock index with crude oil were the highest with a downward trend during the start of the Russian-Ukraine conflict in 2022. The high correlation between these variables indicates that the variables are not suitable for diversification. Meanwhile, the correlation of the US Islamic stock index with gold was the lowest from 2014 until 2022 with an upward trend from the beginning of the pandemic. Even though it shows an upward trend, gold still has the lowest correlation compared to other commodities, indicating that it is a suitable candidate as a hedging instrument for the US Islamic stock index. The correlation between the US Islamic stock index and Bitcoin has been stable from 2014 until 2020 when it started showing a downward trend. The downward trend signifies an opportunity for diversification of the variables. Bitcoin has positive correlation from 2014 until 2019, but since the start of pandemic, it shows a negative correlation with the US Islamic stock index, signifying it is a good safe haven and hedging tool for US Islamic index.

IV. Concluding Remarks

The purpose of this study is to determine the correlations among the US Islamic stock index, Bitcoin, and other commodities like gold and crude oil, during times of turbulence. Based on the MGARCH-DCC model, the study’s results may be summarise as follows.

We discover that the gold price return has the lowest volatility and is negatively correlated with the US Islamic stock index. Thus, an investor exposed to the US Islamic stock index may invest in gold to get diversification advantages. Gold also can be considered a good safe haven and hedging tool for most periods under investigation, except when the pandemic started in 2020 until the beginning of the Russia-Ukraine war conflict in 2022, when it shows a negative correlation with the US Islamic stock index again. Bitcoin may also be used for diversification purposes because the US Islamic stock index has the second-lowest correlation with the cryptocurrency. However, Bitcoin is more volatile than gold, and investors should exercise caution if they decide to include Bitcoin in their portfolios.

Our results also show that the diversification advantages of gold for the US Islamic stock index may be acquired in both good and bad times since the correlation between these two variables is modest. Gold has been proven to be an effective hedging tool throughout history and continues to be so now. This study enables us to appreciate the views of the relatively contemporary approach used in this analysis, enabling us to comprehend portfolio diversification opportunities.

The study’s findings are also important for the government in distributing limited funds and for the policymakers in establishing new policies throughout a range of investment horizons. The US government should address any shocks to the variables under discussion, while formulating macro-stabilisation measures for the Islamic stock index, since failing to do so may result in an economic slowdown or stock market crisis.