I. Introduction

Understanding inflation dynamics in an economy is a crucial issue for policymakers. In this regard, the relationship between inflation and inflation uncertainty has received much theoretical and empirical attention in macroeconomics literature, particularly since the Nobel lecture by Friedman (1977) who argues that an increase in inflation causes monetary authorities to respond unpredictably, increasing uncertainty about the future rate of inflation.[1] Ball (1992) formalizes this idea using an asymmetric information game between monetary authorities and the public. According to Ball (1992), if inflation is low, uncertainty about inflation will also be low since the public believes that the monetary authorities will strive to keep inflation low. On the other hand, if current inflation rises owing to an unforeseen shock, the authorities will adopt a disinflationary policy as they may not be willing to accept the temporary fall in output. Such actions would lead to a rise in monetary policy uncertainty, hence high inflation uncertainty. In the literature, this is popularly known as the Friedman-Ball hypothesis. Later empirical studies such as Bruner & Hess (1993) and Grier & Perry (1998, 2000) provide evidence supporting the Friedman-Ball hypothesis.

In contrast to Friedman and Ball’s hypothesis, Cukierman & Meltzer (1986) argue that policymakers often follow discretionary policies instead of rule-based policies to try to stimulate economic growth. Under such circumstances, a rise in uncertainty about future inflation may cause higher inflation as it incentivizes policymakers to produce an inflation surprise to encourage growth. In contrast, Holand (1995) argues that if the monetary authority strives to reduce the real cost of inflation uncertainty, an increase in inflation uncertainty will lead to lower average inflation. These two contrasting views are popularly known as the Cukierman-Meltzer hypothesis and the Holand hypothesis.

Given this backdrop, this study investigates the relationship between inflation and inflation uncertainty in India. For several reasons, we chose India. First, very few studies have investigated the relationship between inflation and inflation uncertainty. The findings appear to be mixed and ambiguous. For instance, Narayan and Narayan (2013), using the Exponential Generalized Autoregressive Conditional Heteroskedasticity (EGARCH) model, reported evidence supporting Cukierman and Meltzer’s hypothesis. Similarly, Chowdhury (2014), using the Generalized Autoregressive Conditional Heteroskedasticity (GARCH) model, found evidence in favor of the Friedman-Ball and Cukierman-Meltzer hypotheses. Balaji et al. (2016), using Stochastic Volatility (SV) in mean and multivariate GARCH models, found evidence supporting the Friedman-Ball and Holland hypotheses. More recently, Tripathi (2021) reported evidence supporting all three hypotheses. Secondly, we observe that all the existing studies in India use the Wholesale Price Index (WPI) inflation in their analyses (e.g., Balaji et al., 2016; Chowdhury, 2014; Tripathi, 2021). In 2014, the Reserve Bank of India (RBI) replaced the WPI with a new Consumer Price Index (CPI) as the economy’s new nominal anchor. Subsequently, the RBI adopted flexible inflation targeting in 2016, where the annualized CPI inflation rate is targeted at 4% with an upper and lower bound of 6% and 2% respectively. Therefore, empirical analysis using CPI inflation would provide valuable policy-related insights than WPI inflation would. Besides, the Indian economy has gone through several policy reforms and crisis episodes. This might have caused changes in the relationship between inflation and its volatility which needs to be investigated.

Considering the above-mentioned issues, this study uses CPI inflation to unveil the relationship between inflation and its volatility using the Stochastic Volatility in Mean with Time-varying Parameters (TVP-SVM) model developed by Chan (2017), which has a crucial advantage over the existing GARCH and SV models. It allows the parameters of the model to vary over time. In addition, the stochastic volatility of inflation is modeled as an additional regressor in the mean equation, which allows us to capture the time-varying impact of inflation uncertainty on inflation.

The rest of the paper is organized as follows: Section 2 briefly outlines the TVP-SVM model of Chan (2017), Section 3 reports the empirical evidence from our estimated model, and Section 4 concludes the paper.

II. The TVP-SVM model

The SV models developed by Koopman & Hall Uspensky (2002) are widely recognized as better alternatives to GARCH types of models in econometrics literature. The variance in the SV model is a random variable and it changes stochastically. The Kalman filter method is used to estimate such models. The structure of a standard SV model can be written as follows:

yt=x′tβt+αteht+εytεyt∼N(0,eht)

ht=μ+ϕ(ht−1−μ)+εhtεht∼N(0,σ2)

where is the inflation rate, is the vector of explanatory variables, is vector of time-varying parameters. The disturbance and are mutually and serially uncorrelated. The log volatility inflation follows an AR (1) process with The coefficient captures the time-varying impact of stochastic volatility of inflation on the current inflation.

The vector of coefficients, that is are modeled as a first-order random walk process as follows:

γt=γt−1+εγtεγt∼N(0,Ω)

It is important to note that the model will reduce to a TVP regression with a stochastic volatility model if for all ‘t’. The above equations describe a Gaussian state space model, which is linear in and non-linear in Because the model is non-linear, estimation using the Maximum Likelihood method will not provide reliable results for the parameter. Chan (2017) proposes an efficient Markov-Chain-Monte-Carlo (MCMC) sampling method to estimate the model instead of the traditional Kalman filter. Furthermore, to complete the model, he assumes the following independent priors[2] for ,𝜙, and Ω.

μ∼N(μ0,Vμ), ϕ∼N(ϕ0,Vϕ)1(|ϕ|<1)

σ2∼IG(vσ2,Sσ2),Ω∼IW(vΩ,SΩ)

where IG and IW denote inverse Gama and inverse Wishart distribution respectively. indicates imposition of stationary condition on the prior for Following Chan (2017) and Stock & Watson (2007), we decompose inflation into two parts, i.e., trend and transitory, to capture the impact of past inflation on the volatility of inflation. The variance of the trend component is constant, whereas that of the transitory part has stochastic volatility. To capture the effect of past inflation on the current volatility of inflation, following the Friedman-Ball hypothesis, we model as an additional regressor in the volatility equation to capture the effect of past inflation on future inflation volatility. After incorporating the mentioned changes, the final TVP-SVM model can be written as follows:

yt=x′tβt+αteht+εytεyt∼N(0,eht)

ht=μ+ϕ(ht−1−μ)+βyt−1+εht εht∼N(0,σ2)

γt=γt−1+εγtεγt∼N(0,Ω)

where is the vector of coefficients, and captures the effect of past inflation rates on the current volatility of inflation.

III. Empirical Results

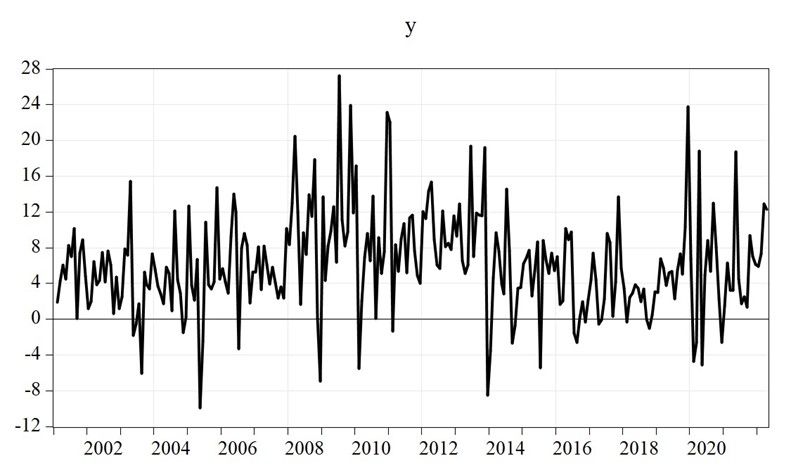

We use monthly data on Consumer Price Index (CPI) from January 2001 to April 2022[3]. The X-13 ARIMA method has been used to correct seasonality issues in the data. Following Grier & Perry (2000), we define the monthly inflation rate as The Augmented Dickey-Fuller and Phillips-Perron tests are then employed to check the stationary properties of The result[4] reveals that is stationary at the levels. Following Chan (2017), we draw 50,000 samples after a burn-in period of 5000. The estimation is done using the efficient MCMC algorithm suggested by Chan (2017). The estimated coefficients of the model with their corresponding confidence band are reported in Table 1. The autoregressive coefficient of the variance is estimated to be 0.91, indicating that volatility of inflation is highly persistent in India. The coefficient is estimated to be positive (0.002) and significant, implying that a rise in past inflation increases uncertainty about future inflation, supporting the Friedman-Ball hypothesis. However, the effect is very limited.

_.jpg)

_.jpg)

_.jpg)

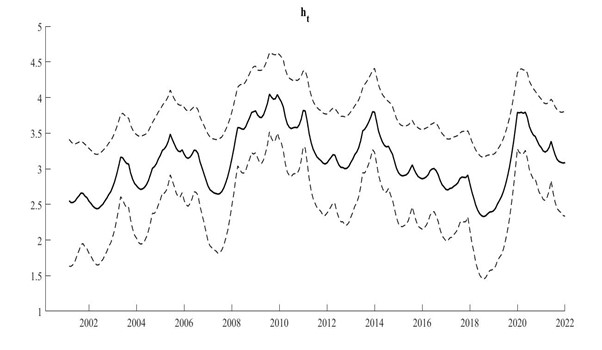

The log volatility of the inflation rate shoots up during major global events and crisis episodes such as the Global Financial Crisis (GFC) of 2008, the oil price rise during 2011-13, the economic slowdown of India which started in 2018, and the most recent Covid-19 pandemic (Figure 2). The impact of inflation uncertainty on inflation rate (Figure 3) is positive and statistically significant throughout the estimation period supporting the Cukierman-Meltzer hypothesis. Between 2005 and 2012, the impact of inflation uncertainty on inflation increased substantially. This particular period is characterized by high inflation volatility episodes, as seen in Figure 3. After 2012, a marginal decline in the impact is observed till 2016. It may be due to the increase in the credibility of India’s monetary policy. A marginal rise in the impact can be observed from 2016 to the end of the estimation period. It may be attributed to the rising volatility of inflation triggered by the economic slowdown that India experienced from 2018, as well as the recent Covid-19 pandemic. The results are consistent with the findings of Narayan and Narayan (2013) and Chowdhury (2014), who find evidence in favor of the Friedman-Ball and Cukierman-Meltzer hypotheses. However, the results, to some extent, contradict the findings of Balaji et al. (2016) and Tripathi (2021), who find evidence in support of the Holland hypothesis. The difference in results may be attributed to the inflation measures used and the methodology employed in the abovementioned studies.

IV. Conclusion

This paper empirically investigates the time-varying nexus between inflation and its volatility uncertainty in India using the TVP-SVM model. The empirical results support the Cukierman-Meltzer and Friedman-Ball hypotheses. From a policy standpoint, the results suggest that to stabilize the inflation rate, the RBI must adopt policies which will address reducing the volatility of inflation. In this context, proper implementation of the inflation-targeting framework is critical to contain the volatility of inflation.

The examples include but are not limited to Ball (1992), Bruner & Hess (1993), and Grier & Perry (1998, 2000).

To know more about the hyper parameter and the posterior drawing process of the parameters, see Chan (2017).

The chosen sample period is based on availability of data. The data on new CPI index starts from January 2011 onwards. Data prior to that were back cast by the RBI using the CPI for Industrial workers which is freely available on their official website.

The result is not reported to save space.