I. Introduction

In this paper, the interdependence between geopolitical risk and stock returns in three main North-East Asian countries of China, South Korea and Japan is examined. The literature linking stock market and geopolitical risks follows different theoretical channels[1] such as (a) real options or the investment irreversibility (b) portfolio diversification and (c) growth options. These are important channels through which uncertainty, such as geopolitical risk, affects economic activities like stock returns. However, among these strands of theories, the investment irreversibility hypothesis is the most relevant to this study as it relates to the channel through which uncertainty affect business investment, as firms will usually delay their investment until some of the uncertainties are resolved (Gulen & Ion, 2016). The delays in capital investment will likely deteriorate operating firms’ growth stability and later lead to a decline in firms’ stock prices.

The literature on geopolitical risk and stock market returns has developed over time[2] with varieties of estimation techniques that have produced mixed findings. For instance, Hoque et al. (2020) analyze a monthly series spanning January 2003 to December 2017 and find that geopolitical risk has an asymmetric effect on the stock markets of different countries. In support of that same result, Cheng & Chiu (2018) report evidence of economic contractions for differential response of the stock market to geopolitical risk for 38 emerging countries. In contrast, Balcilar et al. (2018) find that geopolitical turmoil unfavorably affects stock returns in BRICS countries, while Alqahtani et al. (2020) provides empirical evidence to support a positive predictive power for geopolitical risk for stock markets.

Furthermore, the debate on geopolitical risk and stock returns has not been settled due to its implications on investment decisions and its dynamics on financial system exposures and risks (Adeleke et al., 2022; Adeleke & Awodumi, 2022). This unsettled debate is due to several contributing factors, including increases in global tensions (such as war, COVID-19, and rising terrorist acts) and the possible effect of geopolitical risk on the financial market as well as its impact on macroeconomic fundamentals like output growth, investment, and employment (Ha et al., 2021; Yang & Yang 2021; Yang et al., 2021). However, this study is motivated to measure the interdependence between stock market return and geopolitical risks in the context of three main North-East Asian countries (China, Japan, and South Korea) for two main reasons. First, these countries have continued to experience various geopolitical risks, ranging from COVID-19, the China-US trade war, and, more recently, the Russian invasion of Ukraine. Second, financial markets of these countries are well-developed with a market capitalization of US$12.25 trillion, US$5.46 trillion, and US$1.77 trillion for China, Japan, and South Korea respectively.[3] Against this recent development, it is interesting to investigate the relationship between geopolitical risk and stock returns in these three well-developed stock markets. Precisely, this study underscores the connectedness between geopolitical risk and stock market returns in North-East Asia. The remainder of this paper is structured as follows. Section II presents the methodology used. Sections III and IV detail the empirical findings and derived conclusions.

II. Methodology

A monthly series that spans the period of January 1991 to September 2022, within an investment irreversibility theoretical framework, is employed. The study assumes a functional relationship between geopolitical risk and stock returns to exhibit a linear relationship as using the Bi-wavelet Coherence analysis. The advantage of this methodology lies in its ability to allow complex information to be decomposed into elementary forms at different frequencies and scales and subsequently be reconstructed with high precision (Grinsted et al., 2004). Thus, the Bi-wavelet Coherence analysis is a methodology for measuring time-series co-movement between two different series in a time-frequency space. The wavelet transform of a real signal defined as concerning the wavelet function is stated as:

P(η,r)=1√r∫∞−∞ϖ′(t−ηr)P(t)dt

Where are the translation and scale parameters. For instance, in the case of China, this study utilizes two series defined as and with continuous wavelet transforms of the form and Following Grinsted et al. (2004), the wavelet coherence is written as follows:

CWTssE,GPRCH(δ,r)=CWTssE(δ,r)CWT∗GPRCH(δ,r)

is as earlier defined in equation (1), while and refer to the position index and complex conjugate respectively. According to Torrence and Compo (1998), cross wavelet power can also be defined as thus showing the wavelet coherence, which can be used as a measure of the local correlation of the two-time series & in the space of time and scale. This technique is easily comparable to coherence in Fourier analysis. The wavelet coherence is then defined mathematically as:

R2(δ,r)=|S(r−1CWTssE,GPRCH(δ,r)|2S(S−1|CWTssE(δ,r)2)S(S−1|CWTGPRCH(δ,r)2||)

in equation (3) is a smoothing operator, without which the wavelet coherence is equal to one at all scales. The coherence squared coefficient varies from 0 ≤ ≤ 1, with the values close to zero implying a weak correlation and movement towards one implying a strong correlation. Therefore, the wavelet coherence square coefficient helps to analyze co-movement or interdependence between two financial time series like stock market prices and geopolitical risks. In this study, the return series of each country’s stock market prices are computed as with price data sourced from www.investing.com, while the geopolitical risk data is obtained from Caldara and Iacoviello (2022) construct.

III. Findings

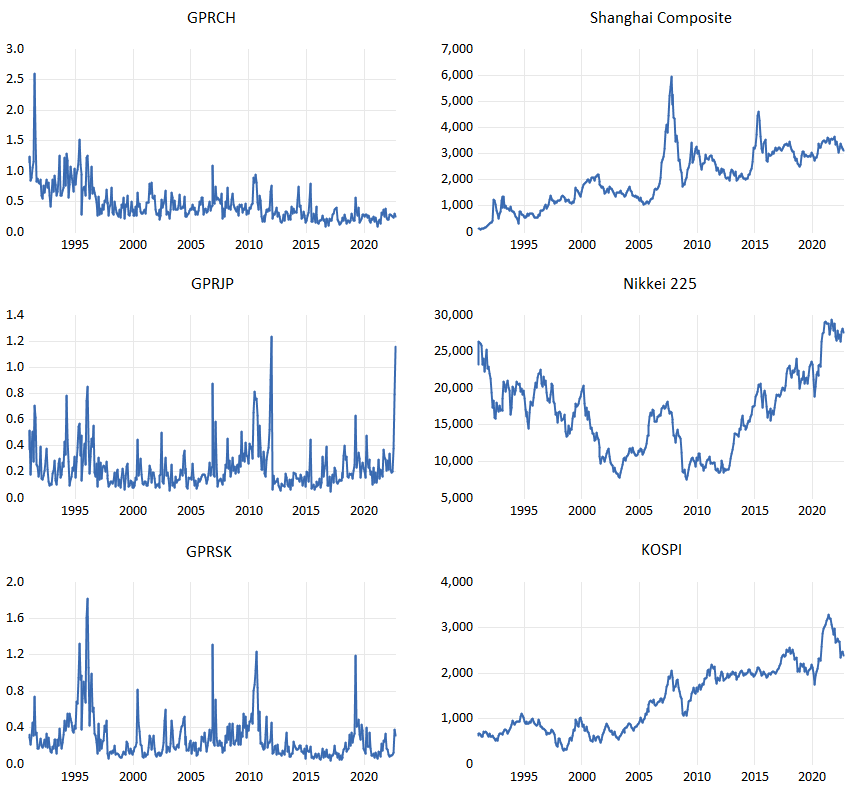

For detailed analysis, this study provides a preliminary analysis of the dataset using descriptive statistics, normality tests, and trend analysis. Table 1 reports the descriptive statistics for the monthly raw and return series of stocks and geopolitical risks across the three selected North-East Asian Countries (China, South Korea, and Japan) from January 1991 to September 2022. China Shanghai Composite (SSE), Japan Nikkei (NIKKEI), and South Korea (KOSPI) stock prices exhibit high-level volatility, while a relatively higher mean value is observed in China, in relation to geopolitical risk. Average monthly returns are observed to be positive for all the series considered. The returns are as high as 101.96, 14.97, and 41.06, and as low as -37.32, -27.216, and -31.810 for China Shanghai Composite (SSE), Japan Nikkei (NIKKEI), and South Korea (KOSPI) stocks, respectively.

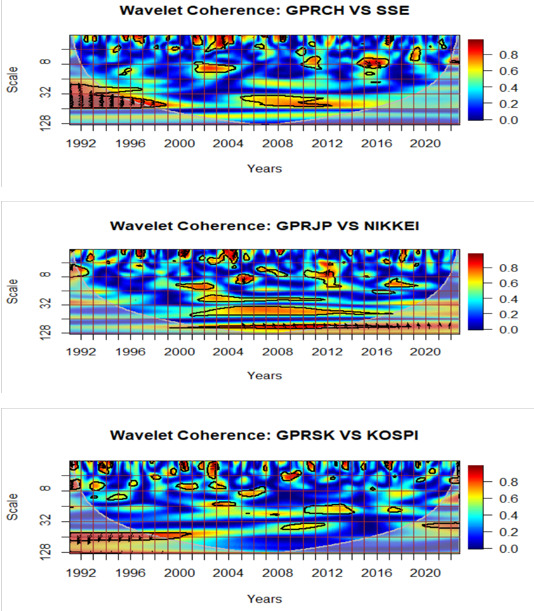

The dynamics of countries’ geopolitical risk and stock market prices are plotted in Figure 1, with a relatively higher stock price fluctuation been observed in Japan and China. Figure 2 shows the Wavelet Coherence diagrams[4] between geopolitical risks (GPR) and Stock Market Returns in three North-East Asian countries. Specifically, Figure 2 illustrates the degree of coherence between geopolitical risk and Shanghai Composite (SSE) returns. The coherence map provides evidence for the existence of the minor mass of strong interdependence at the beginning, the midpoint, and the end of the sample period over 0-16 months’ frequency bands. The presence of many yellow-red vortices in the earlier periods suggests a high degree of connectedness between geopolitical risks and Shanghai Composite (SSE) stock returns. The Chinese stock market seems to react to bad news resulting from the combination of COVID-19 lockdown and the Russian-Ukraine war. Both events signal a loss in value for companies’ stock prices. It is reported that Shanghai Composite Index (SSE) lost 0.9 percent (going from 3,489.24 to 3,458.12 points) on the day of the invasion announcement[5]. These findings reflect that of Yang and Yang (2021) but differ from the findings of Alqahtani et al. (2020) whose research supports a positive link between geopolitical risk and stock markets.

Also, Figure 2 concentrates on the interdependence between geopolitical risk and Japan’s Nikkei 225 (NIKKEI) returns. The results suggest a moderate degree of connectedness between geopolitical risks and the Nikkei 225 return in the earlier months of analysis. The effect appears more visible during the later periods (i.e. between 16 to 128 months) than in the earlier periods, which suggests evidence of a higher effect of geopolitical risk on Japan’s stock market returns. Just as with China, South Korea’s stock returns (see Figure 2) also reflect a high degree of connectedness between geopolitical risk and KOSPI return in the earlier months than in later periods.

IV. Conclusion

This study analyzes the interdependence between geopolitical risk and stock market returns in three North-East Asian countries using monthly frequency data that span the period of January 1991 to September 2022, using a Bivariate Wavelet Coherence. The study establishes that geopolitical risk reduces stock returns. Specifically, this study observed a negative relationship between geopolitical risk and stock returns in the earlier periods in both China and South-Korea (0 to 16 months), while the negative result appears in the later periods in Japan (16 to 128 months). Thus, policymakers and financial sector regulators need to prevent speculation in stock markets that is caused by geopolitical shocks. Also, stock market investors should systematically evaluate the impact of geopolitical risk on stock returns.

See Bloom (2014). Fluctuations in Uncertainty. Journal of Economic Perspectives—Volume 28, Number 2—Spring 2014—Pages 153–176.

The color code for coherency ranges from blue (weak coherency – close to zero) to red (strong coherency – close to one).

https://www.reuters.com/markets/europe/china-stocks-fall-ukraine-crisis-escalates-2022-02-24/