I. Introduction

The coronavirus (COVID-19) epidemic has highlighted the need to better understand the effects of pandemics on international financial markets, including the foreign exchange and stock markets. Pandemic stock market nexus research is based on the theory that investors’ perceptions of risk in the stock market are influenced by both micro and macroeconomic factors (see Haroon & Rizvi, 2020b, 2020a; Narayan, 2019, 2020; Salisu et al., 2020). Like wars, natural catastrophes, and financial crises, pandemics increase market uncertainty, leading to a corresponding spike in risk aversion among investors (see Eichenbaum et al., 2020; Haroon & Rizvi, 2020a; Qadan, 2019; Salisu & Akanni, 2020).

The COVID-19 pandemic has caused global financial markets to experience increased risks driven by fear (Ali et al., 2022; Baker et al., 2020; Okorie & Lin, 2021; Salisu & Akanni, 2020). As a result, investors have suffered losses due to panic-driven selling of stocks (Phan & Narayan, 2020; Shen et al., 2020). It is important to note that emerging stock markets are characterized by low liquidity, high volatility, and reliance on short-term debt markets. These factors make them more susceptible to market inefficiencies and vulnerable to investment losses and crises.

Several studies have investigated the effects of the COVID-19 pandemic on financial markets. Notable research includes the work of Ashraf (2020), Akhtaruzzaman et al. (2020), Phan and Narayan (2020), He et al. (2020), Mishra et al. (2020), Salisu and Sikiru (2020), Salisu and Vo (2020), Topcu and Gulal (2020), Zaremba et al. (2020), and Usman and Nduka (2022). While there have been various studies, only a few have specifically examined the impact of COVID-19 on stock market performance. Noteworthy contributions in this area include the studies conducted by Ashraf et al. (2020), Haroon et al. (2020a), Zaremba et al. (2020), and Zhang et al. (2020). It is important to note that some of these studies have provided preliminary findings, focusing either on individual countries or groups of countries. For instance, Akhtaruzzaman et al. (2020) examined the G7 countries, while Baig et al. (2021) and Caporale et al. (2022) focused on the United States.

There is a lack of empirical research examining the effects of COVID-19 on developing stock markets. Moreover, studies focusing on emerging stock markets have primarily concentrated on the stock performance of enterprises in China and India, as evident in the works of Al-Awadhi et al. (2020), Gu et al. (2020), He et al. (2020), and Mishra et al. (2020). However, a few studies have explored groupings of emerging economies. Notably, Haroon and Rizvi (2020b) and Topcu and Gulal (2020) have delved into this aspect. Topcu and Gulal (2020) discovered that the negative impact of COVID-19 on emerging stock markets gradually diminished by mid-April 2020. Conversely, Haroon and Rizvi (2020b) observed that the increasing number of confirmed coronavirus cases exacerbated the liquidity situation in emerging stock markets. These contradictory findings emphasize the necessity for further investigation into the influence of the pandemic on the stock markets of emerging economies.

This study aims to analyze the stock market performance before, during, and after the COVID-19 pandemic. By focusing on a group of emerging economies, it seeks to enhance our understanding of the financial implications of infectious diseases on developing stock markets. Currently, there is a dearth of research investigating the lasting impact of COVID-19 shocks on stock prices in emerging economies, making this study a valuable contribution to the existing literature. The inclusion of four countries in the analysis provides an advantageous opportunity to compare and contrast their experiences, enabling the formulation of policy inferences based on the study’s findings.

The paper is organized as follows: Section II presents the methodology, section III covers the estimation and results, and section IV offers some concluding remarks.

II. Methodology

Persistence may be defined as the tendency of a series to revert slowly to its long-run/equilibrium level following a shock. To capture persistence, our modelling approach is based on the concept of fractional integration, which, in contrast to the traditional framework, only permits integer degrees of differentiation. Fractionally integration approaches have become more popular for this purpose. Granger & Joyeux (1980), Granger (1980), and Hosking (1981) established the basis for fractionally integrated models. Parke (1999) has provided theoretical justification for shock length using an error-duration model. Some other helpful empirical applications of fractional models may be found in the works of Baillie & Bollerslev (1994) and Gil-Alana & Robinson (1997) .

Granger and Joyeux (1980) introduced the autoregressive fractionally integrated moving average model, which allows for the modelling of persistence or long memory d, where d is a differencing or memory parameter. Therefore, a time series follows a fractional process if:

ϕ(L)(1−L)d(xt−μ)=Θ(L)εt

where, and are the autoregressive and moving average polynomials respectively, is the backward-shift operator and The fractional differencing lag parameter is expressed by the polynomial expansion:

(1−L)d=∞∑k=0Γ(k−d)LkΓ(−d)Γ(k+1)

The gamma function is represented by A fractional process is said to be stationary and invertible when the persistence parameter is - Hence, the autocorrelation function for a zero-integrated process decays geometrically, while the autocorrelation function for a long-memory process decays hyperbolically, and the autocorrelation coefficients have the same sign as Specifically, when we refer to this phenomenon as anti-persistent memory since the autocorrelations are negative. Secondly, for the process is stationary but has a long memory, and shocks decay hyperbolically rather than geometrically. In addition, when the relevant series in question is non-stationary, with mean reverting tendencies and an unconditional variance growing slower than when the persistence parameter Finally, when the procedure is characterized as explosive non-mean reverting and non-stationary.

We utilized the maximum likelihood estimator, a parametric method pioneered by Sowell (1992), to estimate the long-memory (fractional integration) parameter, of a time series. The precision of the parameter estimations generated from the data is a benefit of Sowell’s (1992) method.

III. Estimation & Results

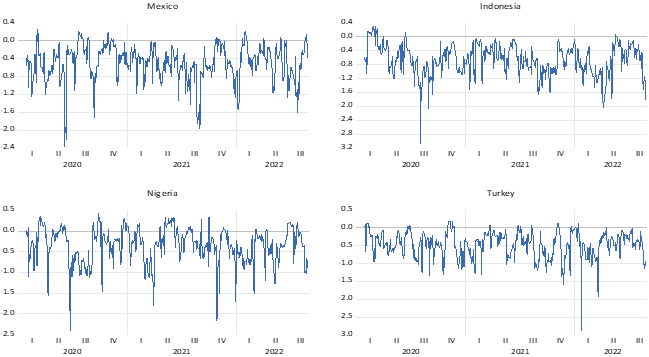

We examined four seasonally unadjusted stock market indices for MINT (Mexico, Indonesia, Nigeria, and Turkey) countries. The series was taken daily from January 2011 to September 2022. Our goal was to analyze the possible impact of the COVID-19 pandemic on the parameter d, a measure of persistence for stock prices. First, we estimated the model up to December 2019 (just before the pandemic), and subsequently used recursive methods to investigate d from January 2020 onwards (during the pandemic). Table 1 exhibits d for the sample period ending in December 2019. We evaluated the stock market series under two specifications: (i) an intercept alone and ii) an intercept with a linear time trend.

The Efficient Market Hypothesis (EMH) proposed by Fama (1970) suggests that stock prices can only be predicted by analyzing historical data. According to this hypothesis, factors like macroeconomic policies and other considerations do not have an impact on the market. In an efficient market, returns are unpredictable, while in an inefficient market, investors can make abnormal returns.

To examine the efficiency of a stock price, researchers often test for the presence of long memory. The null hypothesis assumes no long memory in the market while the alternative hypothesis suggests fractional integration However, recent evidence has indicated a violation of the strong form of the Efficient Market Hypothesis. This necessitates a more thorough investigation into whether a stock or indices, despite exhibiting long memory, is stationary. When the fractional integration parameter falls between zero and half (i.e., it indicates a situation where market shocks fade away quickly. The market may still be considered efficient but in a weakened form of the EMH. On the other hand, when non-stationary stock market indices display mean-reverting behavior and has long memory. In this scenario, markets are inefficient and risky because the effects of system shocks may persist for a prolonged period, assuming the persistence is not permanent

Table 1 reports the estimates of the fractional integration parameter for various MINT countries’ equities. We find strong evidence in favor of fractional integration in returns in Indonesia and Nigeria. In Indonesia, equities were found to display anti-persistence or long-range negative dependence as the autocorrelations are negative. For Nigeria, equities displayed long memory with shocks decaying hyperbolically. However, the results of Mexico and Turkey were insignificant. Recursively, we re-estimated the differencing parameter to account for the COVID-19 pandemic. We added one observation daily from January 2020 until September 2022. Figure 1 displays the findings. The differencing parameter was relatively unstable during the COVID-19 period, suggesting that the pandemic had an impact on the level of stock price persistence in MINT countries.

IV. Conclusion

This paper presents a novel perspective on the relationship between COVID-19 and stock markets, focusing on the MINT countries. Specifically, it investigates the persistence of COVID-19 shocks on stock prices to assess stock market efficiency. The study employs a fractional unit root approach with two specifications: one with an intercept and the other with an intercept and a linear trend. The sample period is divided into two parts, pre-COVID-19 and during the pandemic.

The findings reveal that the Efficient Market Hypothesis (EMH) does not hold for Nigeria and Indonesia, as their stock prices exhibit fractional integration. However, the results for Mexico and Turkey are statistically insignificant. While the coefficients for Indonesia and Nigeria suggest market inefficiency, each country presents unique characteristics. For instance, Indonesia’s stock market demonstrates long-range negative dependence, indicating that market shocks persist for extended periods, and future prices depend on past market behavior. On the other hand, the parameters for Nigeria suggest weak-form efficiency, implying that although the market exhibits long memory, shocks dissipate quickly, and stock prices are random, not necessarily influenced by previous market patterns.

Analyzing the COVID-19 period reveals that the pandemic has influenced the level of shock price persistence in the MINT countries. This suggests that the pandemic has heightened stock market inefficiency in the sampled countries. Overall, the findings suggest that due to market inefficiency, arbitrage and speculation are likely to play prominent roles in these markets.

Disclosure

Views expressed in this paper are those of the authors, and not necessarily those of the Bank of England, Central Bank of Nigeria or their respective policy committees.